- Has open mind about the precise scale of the monetary policy tightening that will be needed.

- Calibration of the monetary policy stance needs to be regularly reviewed in line with the incoming information

- Says ECB will have data-dependent, meeting-by-meeting approach to setting interest rates

- monetary policy poses two-sided risks to the delivery of our medium-term inflation target

- It is fully priced (in line with our expressed policy intentions) that the main policy rate (the DFR) will reach 300 basis points in March, and it is priced to rise even higher subsequently

- If the increasing role of intangible assets for firm revenues turns out to be a persistent trend, it could support higher interest rate sensitivity, since an increasing role of intangible assets means equity valuations may turn out more sensitive to interest rate changes than in the past

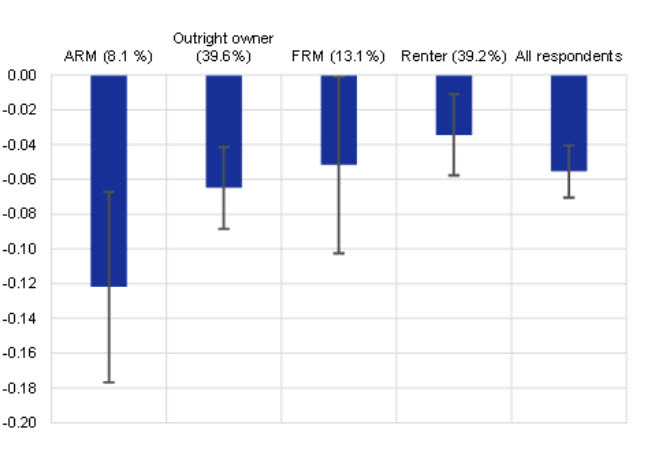

It's a long speech but two things stand out for me, one is that eurozone household will be largely immune from hikes via the mortgage channel with nearly 80% either renting or owning their homes outright. Just 8.1% are on adjustable rate mortgages.

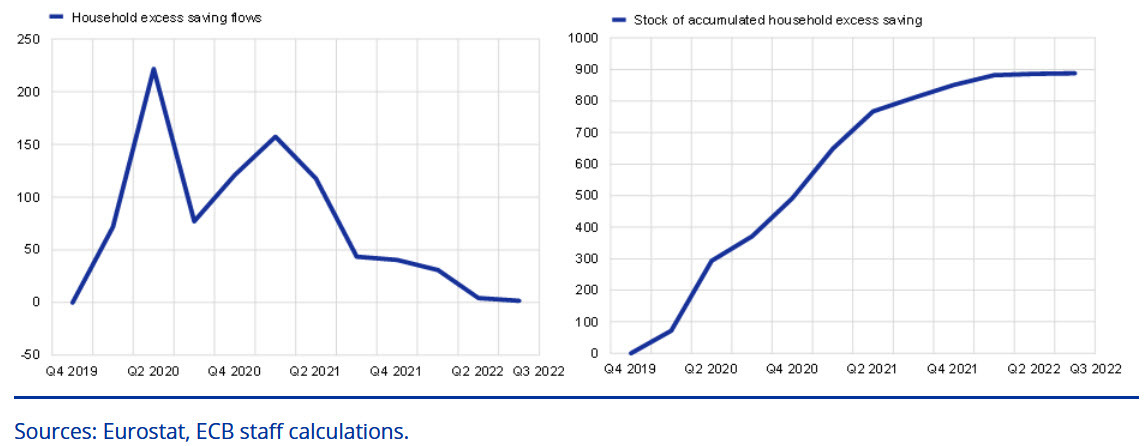

Secondly, the consumer is still flush with pandemic savings with very little drawdown as of the end of Q3.

Lane noted that this will act as a buffer for consumption but noted that a large share of it accrued to the wealthiest households and that much of the money that went to low income households could be swallowed up by food and energy costs.

Overall, there are some interesting observations on the nature of the eurozone economy here but nearly nothing to signal what's coming next in monetary policy.