The volatility playbook for the week ahead

After a week where markets have had to try and understand the potential fallout on the Chinese economy from the coronavirus outbreak, a more dovish BoC, a reasonable Aussie jobs report, and solid UK data, we head into the new week with a number of moving parts through which to navigate.

One

aspect that I have addressed in the 'Week Ahead' playbook is the message I am

seeing from the US bond market and it is a play that is progressively

suggesting more risk averse positioning. It gives me some belief that implied

volatility in markets could start to respond and move higher. I have mentioned

in reports of past that the bond market has never fully bought into the

reflation trade that so many economists had got quite excited about going into

2020. Where, if I look at the long end of the US Treasury or German bund curve,

or even the copper/gold ratio, the market is saying reflation is a pipe dream,

and instead, we may actually be too optimistic about the global growth story.

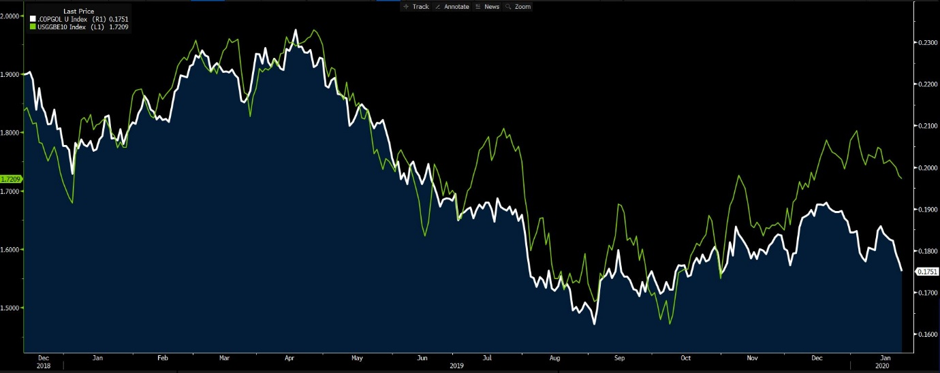

(Green - US 10-year inflation expectations,

white - copper/.gold ratio)

We

know the FOMC meeting is this coming week and while no one expects a change in the

fed funds rate, we are expecting Jay Powell to be intensely probed about the

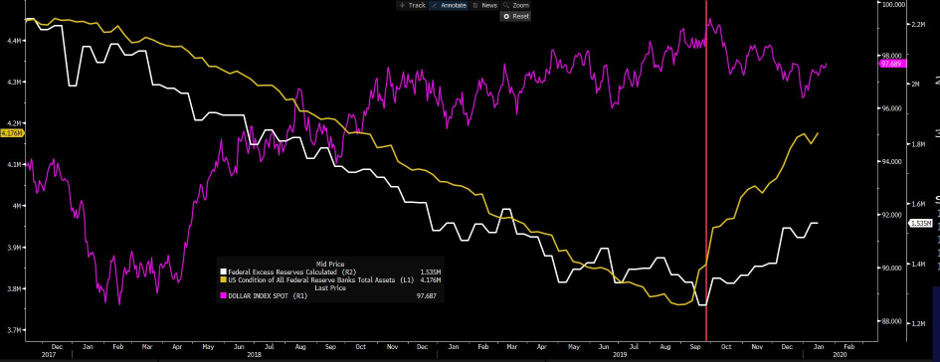

Fed's balance sheet and measures to support the repo market. Risk markets, such

as equities, have been supported by changes to excess reserves, which despite

calls to the contrary from the Fed, the market has taken these changes as QE,

and this may well be coming to an end - or, should I say, the expansion of

reserve growth will soon abate.

(White - excess reserves,

yellow - Fed's balance sheet, purple - USD index)

While

incredibly simplistic, if excess reserves are not increasing, does this mean

risk takes a breather?

A break lower in real (inflation-adjusted) yields

could also result in a flatter bond curve, with implied volatility kicking-up a

touch, as modest risk aversion stemming from the virus outbreak takes hold. We

will continue to be focused on the contagion in China and while I am no

virologist, it just seems that when you effectively quarantined 12 million of

people there must be unforeseen consequences.

The parallels with 2003 SARS outbreak have been

made and the moves higher in USDCNH (and lower in CHFJPY) are telling me the PBOC

are expected to support economics. Consider that in 2003 we saw Chinese retail

sales fall from 9.3% in March to 4.3% in May, and this is the playbook we have

to contrast. This situation obviously has further to play out in markets, and

the risk to the economics and the oil market is growing.

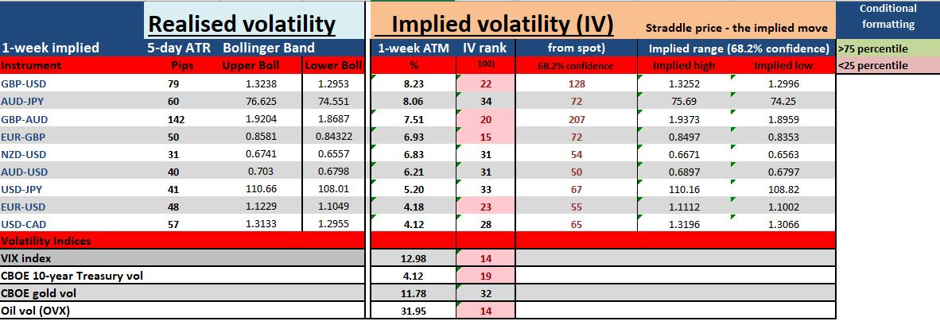

In the video I also focus on Aussie Q4 CPI and the

BoE meeting which will get strong attention from market participants. Somewhat

surprisingly, 1-week implied vols are still subdued, and while buying vol has

been a poor trade, I would expect these ranges to be tested and this plays into

position sizing and risk considerations.

(Implied

volatility matrix)

Have a great weekend to all and happy Chinese New Year,