Greetings one and all

Anyone back the winner in the Melbourne Cup?

RBA on hold but all/most eyes were on the race course anyhow which could account for the immediate volatility around the announcement

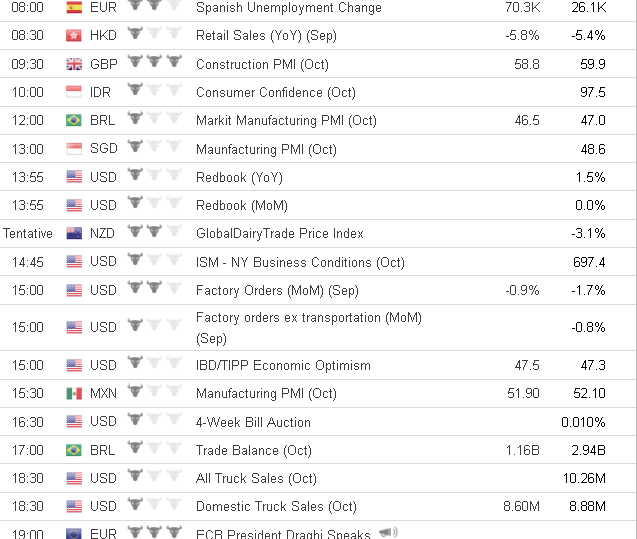

Data wise today it's UK construction PMI and US durable goods that provide the highlights on what is essentially a thin day with attention turning towards the UK inflation report and MPC plus US NFPs later this week

As always I wish you a good session

Times GMT