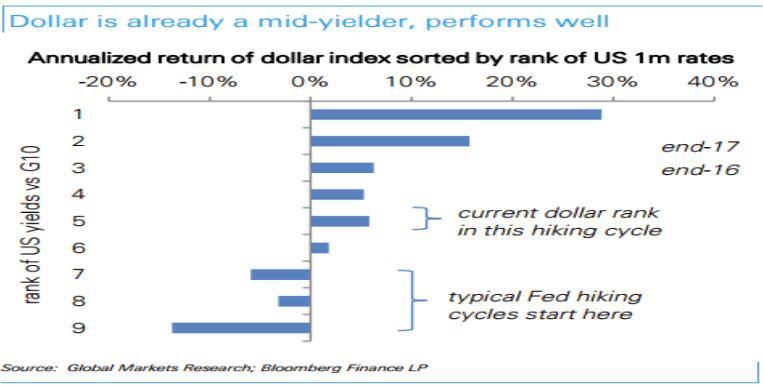

1- Dollar a high-yielder soon: "A striking pattern of

previous Fed hiking cycles is that the dollar has weakened following the

first FOMC rate increase. The most likely reason is that US yields have

ranked in the bottom-3 or below at the start of all major Fed hiking

cycles since the 1980s. Low-yielding status is historically associated

with significant dollar depreciation, even as rate differentials have

widened in favour of the USD as the rate cycle unfolded. This Fed cycle

is unique because the dollar is already and remarkably a mid-yielder

compared to the rest of the world: US short-end rates are currently

higher than half of G10 FX, and assuming current forwards are realized

(2 Fed hikes this year) the USD will become a full-fledged high-yielder

by the end of the year. A highyielding dollar leads to significant

dollar outperformance based on past experience, making the ranking of US

yields an important dollar supportive factor in 2016 (chart 1)," DB

argues.

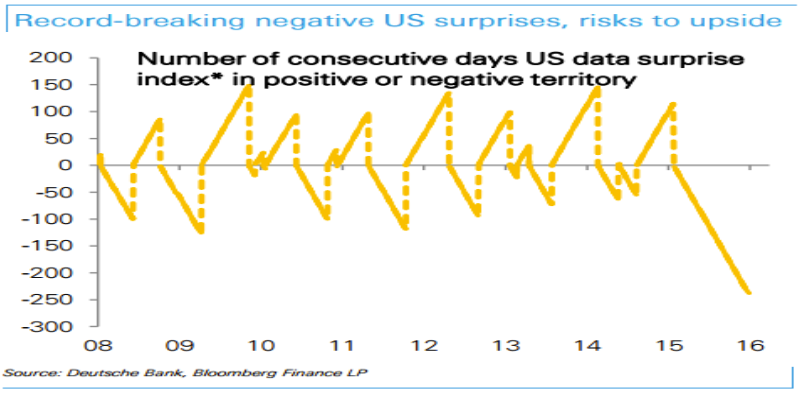

2- Risks skewed toward better US data. "Another unique

part of the current Fed hiking cycle is that it has started at a time of

disappointing US data releases. The last year has seen the longest run

of uninterrupted negative US data surprises going all the way back to

the early 2000s (chart 2). Similarly, the number of economists expecting

3%+ growth this year has dropped to a new post-crisis low according to

the Philly Fed survey of professional forecasters. The odds are

therefore skewed the other way. Even if it will only take two Fed hikes

to make the dollar a high-yielder, there are upside risks to both growth

expectations and the number of Fed hikes that are priced in," DB adds.

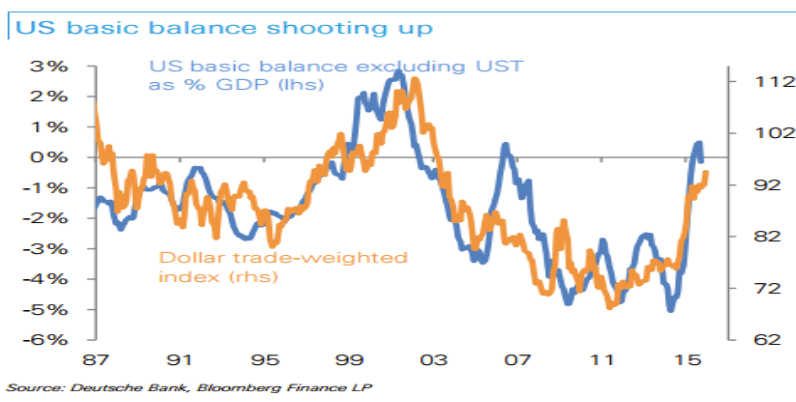

3- Portfolio flow unique as well. "Typical dollar bull

runs have been accompanied by a significant rise in foreign US inflows.

But there is something unique about the current portfolio cycle as well.

The USD is currently benefitting from large repatriation of assets by

American investors, whose selling of foreign securities is running at an

all time high. This is driving the US private basic balance to the

highest levels in almost two decades, which is suggesting that the US

TWI is in-line with portfolio flow trends. The dollar's reliance on

repatriation makes American portfolio preferences the most important

factor behind the current dollar up-cycle. It is the dearth of

investment opportunities abroad rather than renewed foreign interest

that is driving dolar strength," DB notes.

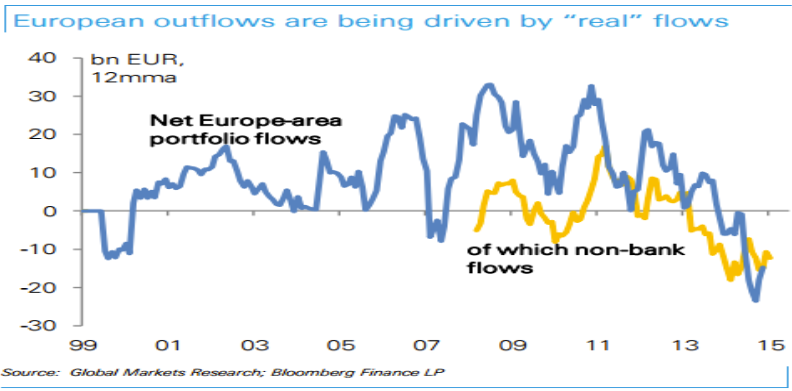

4- Europeans abandoning Europe. "On the other side of

the Atlantic the recovery remains intact but the euro has not been

responsive to better European data. Ongoing ECB dovishness, negative

yields, and European investors' large underweight in foreign assets all

suggest that these outflows are likely to continue, a phenomenon we have

previously termed Euroglut. Interestingly, the composition of portfolio

flows between different investors has undergone a significant

transformation over 2015. Non-bank portfolio flows have become the

dominant portion of Euro-area capital outflows, suggestive of underlying

shifts in European investor preferences rather than changes to bank

balance sheets that are also typically hedged (chart 4)," DB adds.

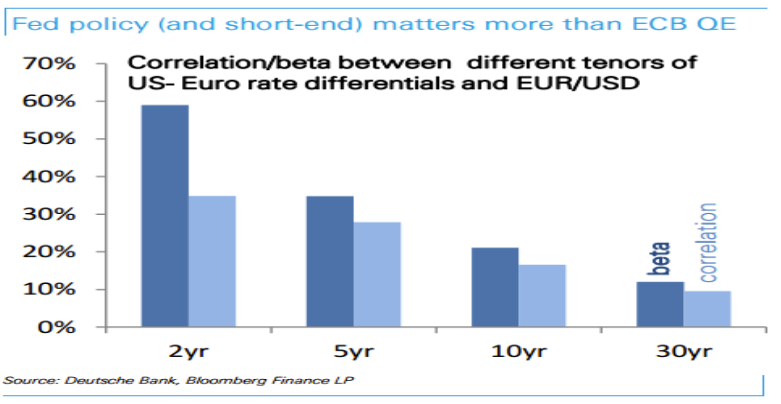

5- ECB taper not important as Fed rate hikes. "Persistent

weakness in the oil price and downside surprises to inflation suggest

that the risks are skewed toward more ECB easing this year. But could a

decision by the ECB to taper its QE purchases later mark the end of the

EUR/USD bear run and by extension the long-term dollar up-cycle? It is

doubtful this would be the case because ECB decisions on QE are more

relevant for the long-end of the European curve rather than near-term

rate expectations. The latter in turn exert significantly higher

influence on FX (chart 5). So long as the European short-end remains

anchored, it will be the pace and timing of the Fed cycle that will

dominate dollar drivers rather than the pace of ECB QE," DB argues.

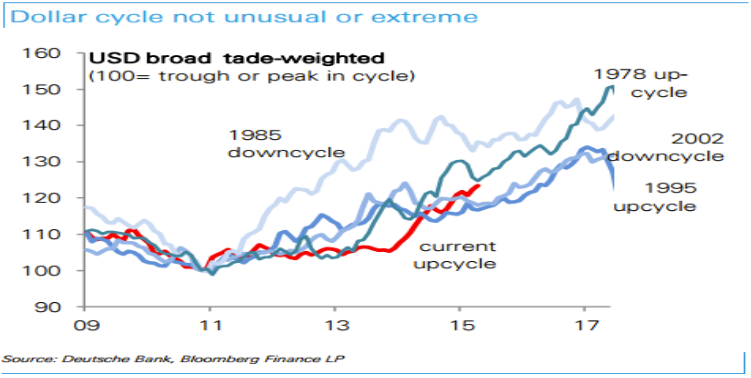

6- China and risks to dollar outlook. "The biggest risk

to our dollar view is a significant slowdown in the US economy that

stops (rather than decelerates) the Fed hiking cycle and potentially

brings easing back on the table. Beyond that, portfolio flows, relative

central bank cycles, and China's recent willingness to tolerate more

dollar strength all suggest the dollar has more scope to appreciate in

2016. The latter is particularly important because past USDCNY stability

has prevented the broad trade-weighted dollar from appreciating as much

as the narrow index given China's high weighting. Given our ongoing

bearishness on RMB (see theme 7) we therefore prefer the broad over the

narrow trade-weighted dollar, which also remains cheaper on account of

CNY valuations. Indeed, even if the current dollar rally is faster than

the late 1990s, it remains well within the bounds of previous dollar

cycles," DB adds.