January and February are the least-important months for the US consumer and wintery weather likely kept shoppers sidelined more than usual this year. Some of the headlines in the retail sales report beat estimates but the overall tone was weakness. To recap:

- Overall retail sales grew 0.3% compared to 0.2% expected but January sales were revised to -0.6% from -0.4%

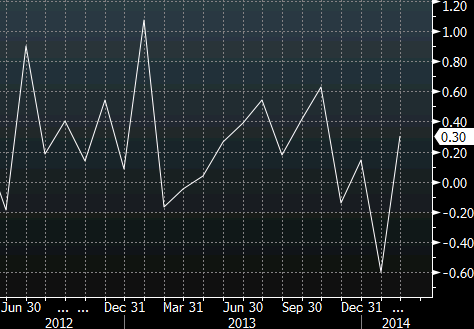

- Excluding autos and gas also grew 0.3% compared to 0.2% expected while the prior was revised to -0.5% from -0.2%

- The control group, which strips out autos, gas and building supplies, was up 0.3% compared to 0.2% expected but the prior was revised to -0.6% from -0.3%

retail sales control group

With the revisions, January was the worst month since June 2012. Over the two-month period, sales were certainly weaker than expected. The lone areas of strength were health & personal care (+1.2%) and sporting goods (+2.5%) and neither is a bellwether of economic confidence. One line that often signals economic optimism is furniture sales which grew just 0.4% after three months of sharp declines.

After the report, economists at Goldman Sachs, Morgan Stanley, Barclays and Credit Suisse all lowered tracking estimates for first quarter growth. Goldman cuts its estimate to 1.5% from 1.7%; at the turn of the calendar Goldman was forecasting 3.0% Q1 growth. Even more dramatic, Morgan Stanley is now forecasting just 0.9% growth in Q1 from 1.9% before.

Bottom line: Weather is still the main story and the market is looking beyond February data but traders will be extremely sensitive to March numbers. If there isn’t a quick turn toward upbeat economic data, worries will quickly mount and risk trades will slump. The initial jobless claims report is a good sign.