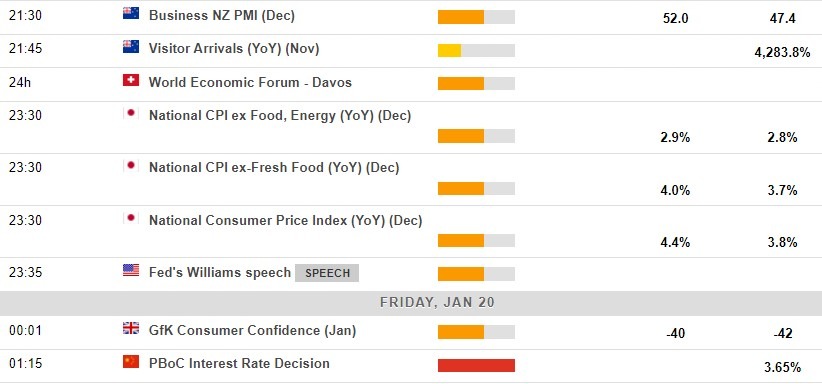

We had the December inflation data for the Tokyo area a couple of weeks again, still on the up:

Today it's the nationwide data for December, which is expected to be higher also. We had the Bank of Japan statement on Wednesday this week, with no incremental move on the JGB ceiling as was expected by some in the markets. The next BOJ meeting is not until March 9 and 10, by which time we'll have had February CPI data also. So this data today is unlikely to have too much impact, but it won't float past unnoticed either. Higher CPI will be a tailwind for the yen, and a headwind for JGBs, and vice versa

Also on the docket is the rate setting from the People's Bank of China. Given the MLF back on Monday was at an unchanged rate:

the 1- and 5-year Loan Prime Rates (LPRs) are expected to be unchanged also. There is a small chance of a cut to one or both. If there is to be a cut then a reduction to the 5 year rate seems most likely (famous last words) as it's a bit of a reference rate for mortgages in China and authorities in the country have been busy rolling out supportive policy for the property sector.

Current LPRs are:

- 3.65% for the one year

- 4.30% for the five year