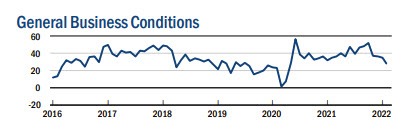

Overview: Overall business activity was little changed. New orders and shipments were steady. Unfilled orders increased. Labor indicators were solid. The inflation data remains high with the prices received reaching a new record high.

Future plans for capital and technology spend remained strong. Nevertheless, the forward looking optimism dipped to the lowest level since mid 2020.

- Prior month came in at -0.7% vs 25.0 expected (big miss last month)

- General business conditions 3.1 versus 11.9 estimate

- New orders 1.4 versus -5.0 last month

- Shipments 2.9 versus 1.0 last month

- Employment 23.1 versus 16.1 last month

- Average employee workweek 10.9 versus 10.3 last month

- Unfilled orders 14.4 versus 12.1 last month

- Inventories 11.7 versus 10.3 last month

- Prices Paid 76.6 versus 76.7 last month

- Prices received 54.1 versus 37.1 last month

The forward looking Indicators showed that while firms expected conditions to improve over the next six months, optimism dipped to its lowest level since mid-2020. The capital expenditures index remained near a multi-year high, suggesting that firms plan significant increases in capital spending.

6-month forward business conditions dips to mid 2020 levels

- General business conditions 28.2 versus 35.1 last month

- new orders 32.9 versus 32.9 last month

- Shipments 32.6 versus 29.3 last month.

- Employment 25.9 versus 29.9 last month

- average employee workweek 15.3 versus 13.8 last month

- prices paid 70.3 versus 76.7 last month

- prices received 51.4 versus 62.1 last month

- capital expenditures 37.8 versus 39.7 last month

- technical spending 29.7 versus 31.9 last month

To access the full report, CLICK HERE