All the angst in markets around the war in Ukraine, inflation Fed rate hikes is drowning out what could be the single-largest catalyst for a sharp slowdown in global growth: China.

Everything is suddenly going wrong in China as a confluence of events threatens to undercut anything close to Beijing's target of 5.5% GDP growth this year.

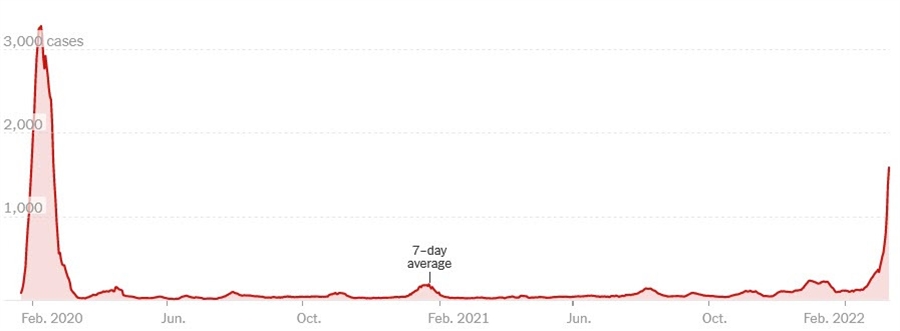

1) Covid outbreak

Covid cases in China are at a two-year high. The nightmare scenario is that something like Hong Kong unfolds where a handful of cases has exponentially risen to +30,000 per day and completely uncontrolled spread.

The province of Jilin (population 24 million) has gone into lockdown along with Shanghai and Shenzhen. I've been surprised by China's ability to suppress various waves of covid but omicron is the toughest test yet with 27 of 31 provinces reporting local a total of 2125 cases.

2) Commodity inflation

There's a temptation to view emerging markets as monolithic but the #1 distinction in my mind is between the commodity exporting emerging markets (LatAm, Africa, Middle East) and the commodity importers (India, China, Turkey). That divergence will be blown open in the year ahead as money flows from the former category to the latter. China is vulnerable socially to high commodity prices.

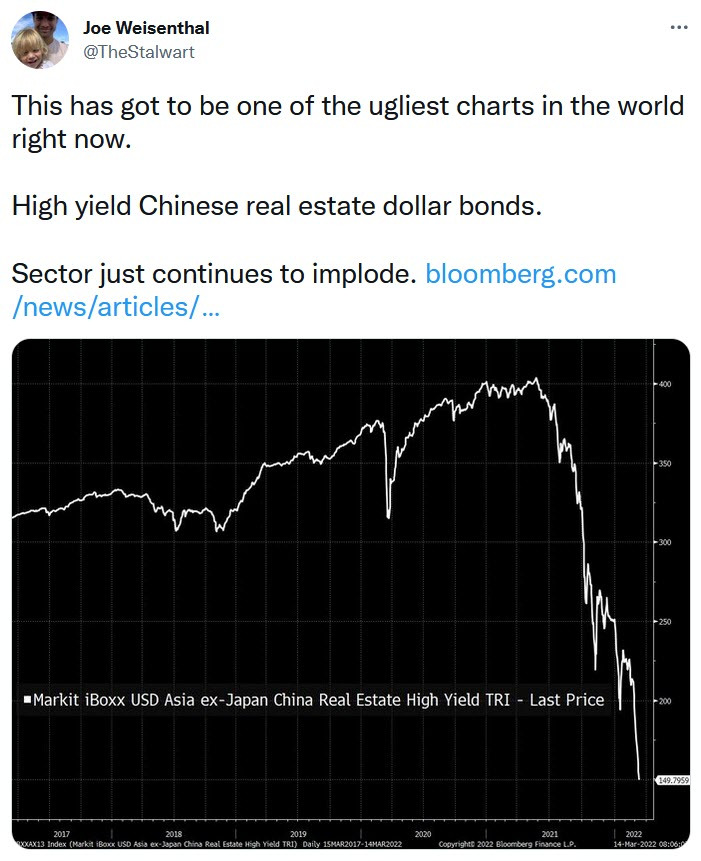

3) Property market

The implosion of Evergrande last year had everyone watching China for signs of contagion and when it didn't happen quickly, the market lost focus. The pain is worsening. In January, sales of land parcels by local government officials were down 72% y/y in value. The losses are reverberating throughout the sector with bonds now yielding upward of 25% and prices have fallen in 14 straight days.

4) China tech implosion

KWEB is the US ETF that tracks Chinese tech stocks.

There's a tech washout globally but Chinese tech stocks are getting hit doubly because of the emergence of the Great Firewall. US tech is being cut off from China and vice versa. The peak of this came right around the time Jack Ma disappeared and that has since signaled that Chinese tech firms would be working for the state, not for shareholders.

5) Central bank jam

High commodity prices and global inflation tie the PBOCs hands. With the headwinds in China from covid and the property market collapse, the normal impulse would be to ease policy but rising inflation could stifle that response. There are certainly levers that China can pull on but it's not a straight-forward as it looked a year ago.