- What has today's anxiety meant for the EURUSD, USDJPY and GBPUSD heading into the close

- Tomorrow is historically the single-worst day for US equities of the year. Here's why

- WTI crude oil futures settle at $87.27

- Credit Agricole: Despite rising US rates, the USD underperforms - what's next?

- With a little help from ChatGPT, what are the districts saying?

- Beige Book: Most Districts indicated little change in economic activity since Sept report

- Jordan loses support in second House speaker vote but says he's not dropping out

- Fed's Bowman: Inflation has come down but is still too high

- US sells 20-year bonds at 5.245% vs 5.257% WI

- Reuters poll: 90 of 111 economists see no change in Fed funds rate in November

- Feds Williams: Inflation has come down quite a bit

- More from Fed's Waller: If inflation fell to 2.5%, Taylor rule would say to cut rates

- Representative Jordan loses again

- Fed's Waller: It's too soon to tell if more policy action needed

- Gensler: SEC still speaking with firms seeking spot bitcoin ETFs

- European equity close: Declines near 1%

- US 10-year yields break out to fresh 16-year high. Dollar climbs.

- EIA weekly US oil inventories -4491K vs -300K expected

- US Sept housing starts 1.358m vs 1.380m expected

- Canada Sept housing starts 270.5K vs 240.0K expected

- The CHF is the strongest and the EUR is the weakest as the NA session begins

- ForexLive European FX news wrap: Gold and oil continue to shine, FX muted

The surging yields continue to pressure markets.

- The 2-year yield is trading at 5.223%. That's the high yield since June 2006 when the yield peaked at 5.283%

- The 10-year yield is trading at 4.911% 6.4 basis points. That is the highest level since July 2007. The high yield in 2007 reached 5.289%

- The 30-year yield is trading back below the 5% level of 4.988% after reaching 5.029%. That was still short of the 5.052% reached on October 6, but still close to the highest level going back to July 2007.

- The 2-10 year spread widened to -31 basis points, up 6.6 basis points on the day

- The 2-30 year widened to -22.6 basis points, up 6.0 basis points on the day.

The move higher in rates pressured stocks. The NASDAQ index was the laggard of the major 3 indices. A snapshot of the closing levels shows:

- Dow industrial average -332.59 points or -0.98% at 33665.07

- S&P index fell -58.62 points or -1.34% at 4314.59

- NASDAQ and tumbled minus 219.45.4 -1.62% at 13314.29

Today, Feds Williams, Waller and Bowman all spoke:

- Federal Reserve Bank of New York President John Williams noted that inflation has decreased significantly but still has some distance to go before reaching the target. He expressed a commitment to achieving the inflation target and mentioned the possibility of lowering interest rates in the future. Williams emphasized the need for a restrictive monetary policy to curb inflation but indicated that the path of such policy would be contingent on economic data.

- Federal Reserve's Christopher Waller suggested that it's premature to determine if further policy action is necessary. Waller stated that more policy rate adjustments might be required if demand and economic activity continue at their recent pace but emphasized a cautious approach, waiting to assess the real economy's performance. He noted positive data in recent months regarding employment and inflation goals and expressed patience in monitoring spending patterns. Waller also anticipated the labor market to gradually loosen and emphasized the importance of monitoring inflation reports over the next few months. He mentioned that long-term rate increases could influence the Fed's policy direction and stated that the Fed still has one rate hike penciled in, which would be data-driven. Additionally, he believed that there might be more potential excess consumer savings than currently estimated and hoped that rate hikes would help slow spending and inflation.

- Federal Reserve's Michelle Bowman commented during a Fed Listens event, that inflation has come down but remains elevated. She highlighted the surprising resilience in goods spending, which has continued instead of reverting to pre-pandemic patterns. Bowman also noted that this spending pattern in the U.S. differs from that of other advanced economies, where the composition of goods versus services spending has returned to historical norms. This suggests that the U.S. economic situation may have unique characteristics compared to its counterparts

The Fed's Beige Book was also released ahead of the FOMC meeting on October 31 and November 1. According to the the Fed districts, the U.S. economy displayed a mix of trends. Consumer spending showed variability, while tourism activity continued to improve. Consumer credit quality remained stable and healthy, and real estate conditions saw minimal change, with low home inventory levels. Manufacturing activity exhibited mixed performance, but many Districts reported an improved outlook for the sector. The near-term economic outlook was generally described as stable, albeit with some hints of slightly weaker growth. Expectations for firms reliant on the holiday shopping season were diverse. Labor market tightness continued to ease across the nation, while prices increased at a modest pace overall. Input cost increases for manufacturers slowed or stabilized, whereas services sector firms faced rising costs. Firms expected price increases in the coming quarters, although at a slower rate than in the previous quarters.

Tomorrow the Fed Chair will have the final say (or one of the final says) ahead of the quiet period ahead of the FOMC rate decision on November 1. He will be speaking at 12 noon to the New York Economic Club. With markets already on edge, Adam added to the anxiety by letting us know that October 19 is the single worst trading day for equities in the US. We have that to look forward to.

After the close, Tesla reported a miss on revenues and earnings-per-share

- Revenues came in at $23.35 billion versus $24.10 billion estimate

- Earnings-per-share came in at $0.66 versus $0.73 expected

- Shares of Tesla are trading down -0.89% at $244.70

- Tesla does say they will deliver the 1st cyber trucks in the 4th quarter which may be

Meanwhile, Netflix beat on earnings-per-share and equaled their revenue per share estimates

- Revenues $8.54 billion versus $8.54 billion estimate

- Earnings-per-share $3.73 versus $3.49 expected

- Shares of Netflix are trading at $377.50 up $31.48 or 9.13%

Lam Research beat on the top and bottom lines but their shares are trading sharply lower (go figure):

- Revenues $3.48 billion versus $3.41 billion expected

- Earnings-per-share $6.85 versus $6.12 expected

- Despite the beat, shares are down -3.05% at $622.63.

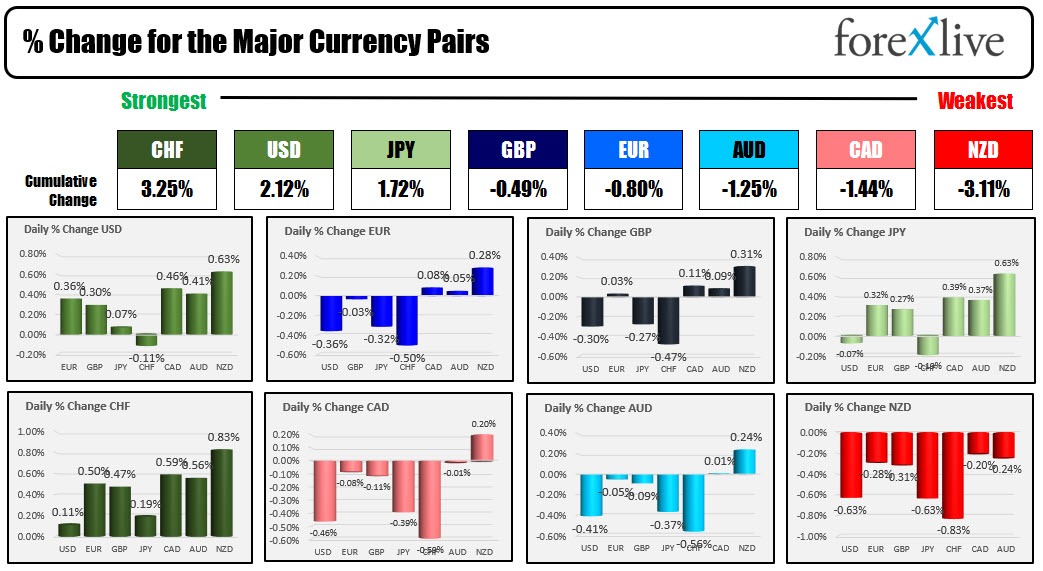

IN the forex market, the traders pushed into the relative safety of the CHF. The USD was also higher. The weakest currencies were the"risk currencies" with the NZD and the AUD being the weakest of the majors. Below is a ranking of the strongest to the weakest as the clock ticks to the end of the day.

For a technical look at the 3 major currency pairs (EURUSD, USDJPY and GBPUSD) as the day comes to the close, click on the video below.