Monday:

The New Zealand Services PMI fell further into contraction:

- 47.1 vs. 48.0 prior.

BNZ Senior Economist Doug Steel commented:

- “The latest PCI readings suggest any bounce through the Q2 GDP figures will be short lived and are consistent with economic contraction returning. In this sense, the PMI and PSI results are more consistent with the RBNZ forecast of a return to recession than the Treasury’s latest forecasts of moderate growth ahead”.

ECB’s Kazimir (hawk – voter) maintains his hawkish views although they are toned down following September hike:

- I wish that September rate hike was the last one.

- But cannot rule out further moves.

- Only via the March forecast next year can we confirm the path towards inflation goal.

- End of rate hikes is to open debate on how to adjust PEPP and APP.

- Once it is clear that no more rate hikes are needed, debate should be on how to speed up QT.

The US NAHB Housing Market Index missed expectations as higher rates are weighing again on the housing market:

- NAHB 45 vs. 50 expected and 50 prior.

- Current single-family home sales 51 vs. 57 prior.

- Sales over next six months 49 vs. 55 prior.

- Prospective buyers 30 vs. 35 prior.

Tuesday:

The RBA released the Meeting Minutes of its September meeting:

- Considered raising rates by 25 bps or holding steady at the September meeting.

- Some further tightening may be required should inflation prove more persistent than expected.

- Case to hold was stronger, recent data did not materially alter the economic outlook.

- Economy still appears to be on a narrow path by which inflation returns to target, employment grows.

- Members recognize the value of allowing more time to see full effects from past tightening on the economy.

- Policy moves will be guided by incoming data and assessment of risks.

- Concerned about productivity growth not picking up as anticipated, services inflation remaining sticky.

- Fuel prices rose sharply in August, could boost headline inflation in Q3.

- Members noted that the labour market remains tight but could be at a turning point.

- Scheduled mortgage payments rose to a historical high of 9.7% of household income in July, set to increase further.

ECB’s Villeroy (hawk – voter) basically confirmed that the ECB is done hiking:

- We will maintain interest rates at 4% for a sufficiently long time.

- The medicine is beginning to work.

- Current ECB rates are at a good level, better to be patient now.

- Once inflation is back to around 2%, rates can fall again.

The Canadian inflation measures beat expectations across the board with the market now seeing a 50/50 chance of another rate hike from the BoC:

- CPI Y/Y 4.0% vs. 3.8% expected and 3.3% prior.

- CPI M/M 0.4% vs. 0.2% expected and 0.6% prior.

- BOC Core Y/Y 3.3% vs. 3.2% prior.

- BOC Core M/M 0.1% vs. 0.5% prior.

- CPI Median 4.1% vs. 3.7% expected and 3.9% prior (revised from 3.7%).

- CPI Trimmed 3.9% vs. 3.5% expected and 3.6% prior.

- CPI Common 4.8% vs. 4.8% expected and 4.8% prior.

The US Housing Starts data missed expectations while Building Permits beat forecasts:

- Housing Starts 1.238M vs. 1.440M expected and 1.447M prior (revised from 1.452M).

- That's the lowest level since June 2020 during the pandemic.

- Building permits 1.543M vs 1.443M expected and 1.442M prior.

BoC’s Kozicki commented on the CPI report and noted that the increase was mainly due to higher energy prices. Their focus is on the underlying measures but even those beat expectations for 3 months in a row already:

- One of the big drivers in August CPI inflation was energy and gasoline prices. They can be pretty volatile.

- It will take a lot of time to sort through the inflation data, given what's going on underneath.

- Energy prices on their own, if it's temporary, is something that gets much less weight because we are concerned about the underlying inflation.

Wednesday:

The PBoC left the LPR rates unchanged as expected:

- LPR 1 year 3.45%.

- LPR 5 year 4.20%.

The UK CPI missed expectations across the board with market now seeing the BoE done with rate hikes:

- CPI Y/Y 6.7% vs. 7.0% expected and 6.8% prior.

- CPI M/M 0.3% vs. 0.7% expected and -0.4% prior.

- Core CPI Y/Y 6.2% vs. 6.8% expected and 6.9% prior.

- Core CPI M/M 0.1% vs. 0.6% expected and 0.3% prior.

ECB’s de Cos (dove – non voter) said that the risks to the inflation outlook are now balanced, which is another way to say that they are done.

ECB’s Makhlouf (neutral – non voter) didn’t want to pre-commit on the next rate decision but he’s of the idea that they have reached the top:

- I do think we are there, or thereabouts, at top of the ladder on rates.

- My view at the moment is that March 2024 is probably too early for 1st rate cut.

- Not saying at our next meeting that we are going to hold, but we are near the top.

- We will have a better sense of 2024 rate profile one we have the next set of projections in December.

The BoC released the minutes of its September meeting:

- The Bank of Canada's Governing Council did not want to set expectations for a rate reduction in the near future, as per the September 6th announcement minutes.

- The Council's discussions revolved around either maintaining the current rates or increasing them.

- Given the uncertain trajectory of core inflation, maintaining a stricter policy should be considered.

- The lack of improvement in underlying inflation is a major worry.

- The Council deliberated if high core inflation might continue even as signs show that restrictive monetary policy is dampening demand.

- Many core inflation metrics appear to be persistent, with little change observed since the July rate announcement.

- There's concern over the proportion of items in the CPI basket that are increasing at an annualized rate exceeding both 3% and 5%.

- The Council anticipates that rising oil and gasoline prices will push inflation up in the coming months.

- The balance between economic supply and demand will play a pivotal role in determining future core and total inflation.

- The large drop in commodity prices will soon be excluded from inflation calculations.

- Governing Council observed that the impact of base-year effects will diminish.

The Fed kept interest rates unchanged at 5.25-5.50% as expected with a hawkish outlook as they kept the terminal rate for 2023 at 5.6% and revised higher the 2024 forecast from 4.6% to 5.1%. Growth was revised higher, unemployment was revised lower and inflation basically unchanged:

- 2023 end of year target rate: 5.6%, unchanged from June.

- 2024 end of year target rate: 5.10% from 4.6% in June.

- Economic activity has been growing steadily.

- Job gains have decelerated but remain robust; unemployment is low.

- Inflation is currently high.

- The U.S. banking system is stable and robust.

- Stricter credit conditions may impact economic activity, employment, and inflation.

- The exact impact of these conditions is still uncertain.

- The Committee is highly focused on inflation risks.

- The Committee's goals are maximum employment and a 2% inflation rate over the long term.

- The Committee will evaluate further information and its implications for monetary policy.

- Factors considered for policy adjustments include the overall tightening of monetary policy, its delayed effects on the economy, and other economic and financial events.

- The Committee plans to reduce its holdings of Treasury securities and other agency debts and securities.

- The primary aim is to bring inflation back to the 2% target.

- The Committee will keep assessing the economic outlook based on incoming data.

- If risks arise that could hinder the Committee's objectives, they are ready to modify the monetary policy stance.

- Their evaluations will consider various data, including labour market stats, inflation trends, financial, and global events.

Moving on to the Fed Chair Powell’s press conference opening remarks:

- Fed is squarely focused on dual mandate.

- Fed has covered a lot of ground, full of facts have yet to be felt.

- We can proceed carefully.

- Our decisions will be based on assessments of data and risks.

- Growths in real GDP has come in above expectations.

- Consumer spending particularly robust.

- Activity and housing have picked up.

- Higher rates weighing on business investment.

- Labor market remains tight.

- Labor supply and demand continue to converge to better balance.

- Labor demand still exceeds supply.

- Expects labor market rebalancing to continue, easing upward pressure on inflation.

- Inflation remains well above our long-run goal of 2%.

- Getting inflation down to 2% has a long way to go.

- Longer term inflation expectations appear to be well anchored.

- Strongly committed to return inflation to 2%.

- Current stance of policy is restrictive, putting downward pressure on economic activity, employment and inflation.

- We are committed to achieving and sustaining sufficiently restrictive policy to bring inflation down to 2% over time.

- Federal Reserve will make decisions meeting by meeting. Federal Reserve is mindful of the uncertainties.

- The Fed is prepared to raise rates further if appropriate.

- Will keep rates restrictive until confident inflation moving down to 2%.

- Reducing inflation is likely to require a period of below trend growth, some softening of labor conditions.

- We will do everything we can to achieve goals.

- Restoring price stability is essential in reaching maximum growth potential.

Q&A:

- The fact that we decide to keep policy rates where it is does not mean we have decided we have or have not reached the stance of policy we are seeking.

- Fed wants to see convincing evidence that we have reached the appropriate level.

- Real interest rates are meaningfully positive.

- Recent labor market report was a good example of what we want to see.

- People want to be careful not to jump to a conclusion one way or the other.

- We are fairly close we think to where we want to get.

- I would attribute huge importance to one hike.

- Stronger economic activity is the main reason for needing to do more with rates.

- It may be that the neutral rate has risen.

- It is plausible that the neutral rate is higher than the longer-run rate.

- I still think there will need to be some softening in labor market.

- In the median forecast don't see a big increase in unemployment, but that is not guaranteed.

- Would not call soft landing a baseline expectation.

- It is also possible the path to soft landing has widened, it may be decided by factors outside our control.

- The fact we've come this far lets us proceed carefully.

- You know sufficiently restrictive only when you see it. It is not something you can arrive at with confidence in a model.

- For now, the question is to try to find a level where we can stay there. We haven't gotten to the point of confidence yet.

- The time will come at some point that it's appropriate to cut, but not saying when.

- Part of the decision to cut may be that real rates are rising because inflation is coming down.

- Strikes, government shutdowns, resumption of the student loan payments, and higher long-term rates are among risks.

- On UAW strike, it could affect output, hiring, and inflation depending on length of strike.

- Government shutdowns don't traditionally have much of a macro effect.

- Energy prices being higher is a significant thing. Higher energy prices sustained can affect inflation and spending.

- The economy appears to have significant momentum.

- A soft landing is a primary objective.

- The worst thing we can do is fail to restore price stability.

- We have the ability to move carefully, and that's what we are planning to do.

- Forecasts are highly uncertain.

- Growth has come in stronger than expected, requiring higher rates.

- The last three readings of inflation have been very good, well aware we need more than three good readings.

- The risk of overtightening and under tightening is becoming more equal, need to find our way to the right level of restriction.

- A possible government shutdown could curtail some of the data we get, we would have to deal with that.

- It looks like we've had a bit of a turn of inflation in June.

- Energy prices don't have that much of a signal about where economy is going.

- If energy prices increase and stay high, it will affect spending, may affect inflation expectations.

- We tend to look through short-term moods and energy prices.

- Rising long-term yields is mostly not about inflation, more about growth supply of treasuries.

- Any decision about future rate cuts will be about what the economy needs.

- We are not looking for a decrease in consumer spending.

- It is a good thing the economy is holding up under rate hikes.

- If economy comes in stronger than expected, it means we will have to do more to bring down inflation.

- Concern number one is restoring price stability.

Thursday:

The New Zealand Q2 GDP came in much better than expected:

- GDP Q2 Y/Y 1.8% vs. 1.2% expected and 2.2% prior.

- GDP Q2 Q/Q 0.9% vs. 0.5% expected and 0% prior (revised from 0.1%).

The SNB left interest rates unchanged at 1.75% vs. 2.00% expected (the market was pricing a 60% chance of a hold):

- Significant tightening of policy in recent quarters is countering remaining inflationary pressure.

- It cannot be ruled out that further tightening may become necessary.

- SNB will monitor inflation developments closely in the coming months.

- Will remain active in the foreign exchange market as necessary.

- Sees 2023 inflation at 2.2% (unchanged).

- Sees 2024 inflation at 2.2% (unchanged).

- Sees 2025 inflation at 1.9%.

SNB’s Chairman Jordan is comfortable with the level of inflation in Switzerland but wary of future risks:

- Inflation battle is not over.

- Given "comfortable" level of Swiss inflation, the best solution is to wait and see.

- Have to see what happens over the next 3 months.

- Clear focus is on price stability.

- We are not reacting to weakening in the economy, but to lower inflation.

ECB’s Kazaks (hawk – voter) didn’t call for higher rates as the ECB is now expected to just keep rates higher for longer:

- Rise in energy prices does create upside risk to inflation.

- Recent energy price rise is structural, not a short-term transitory rise.

- Given current outlook, rate cut expectations around middle of 2024 are too early.

- Rates will need to remain restrictive for quite a while.

ECB’s Nagel (hawk – voter) is another member leaning on the higher for longer stance as he said that “rates must stay sufficiently high for sufficiently long”.

The BoE left the bank rate unchanged at 5.25% vs. 5.50% expected, although the market’s pricing was a 50% chance for both the outcomes:

- Bank rate vote 4-5 vs 8-1 expected (Bailey, Broadbent, Dhingra, Pill, Ramsden voted to hold).

- Underlying growth in the 2H 2023 is likely to be weaker than expected.

- Labour market remains tight by historical standards.

- CPI inflation is expected to fall significantly further in the near-term.

- Monetary policy will need to be sufficiently restrictive for sufficiently long to return inflation to the 2% target sustainably in the medium-term.

- Further tightening in monetary policy would be required if there were evidence of more persistent inflationary pressures.

BoE’s Governor Bailey left a door open for further tightening but the preferred strategy now is to keep rates higher for longer:

- Inflation is falling and we expect it to fall further this year.

- That is welcome news.

- Previous rate hikes are working but inflation is still not where it needs to be.

- There is absolutely no room for complacency.

- Will be watching closely to see if further rate hikes will be needed.

- Will need to keep rates high enough and long enough to get the job done.

- Will do whatever is needed to get inflation back to normal.

- The job is not done yet.

- Not predicting what next bank rate move will be.

- We have got a big job to do yet.

- There is no premature celebration here on inflation falling.

- MPC has not had any discussion about cutting bank rate.

- There are strong views on MPC about inflation outlook.

The US Jobless Claims beat expectations once again by a big margin:

- Initial Claims 201K vs. 225K expected and 221K prior (revised from 220K).

- Continuing claims 1662K vs. 1695K expected and 1683K prior (revised from 1688K).

This report coincides with the NFP survey period.

ECB’s Vujcic (hawk – non voter) is comfortable with the current level of rates:

- As prices ease, the 4% rate will be more restrictive.

- If outlook holds won't need any more rate hikes.

- Latest hike puts us in a better position.

ECB’s Wunsch (hawk – voter) is also leaning towards keeping rates higher for longer:

- Whether we need to do more or not is a very difficult question.

- Have greater confidence that projections can be used as an anchor.

- May have reached a peak in wages, but that's still uncertain.

- Can't conclude yet that we've reached terminal rate.

- I'm fine with reaching inflation target only in 2025.

- Can't exclude a recession, but not the base case.

- Does not see APP sales for now.

- PEPP reinvestments could and earlier than end of 2024.

- There aren't arguments to keep PEPP reinvestments until end of 2024.

- Would be cautious about raising mandatory reserve requirements.

ECB’s Knot (hawk – voter) joins the other hawks in calling the current level of rates sufficient:

- Does not expect a rate hike at next policy meeting.

- Comfortable with current interest rates.

- ECB will stay alert to signals indicating inflation remains too high.

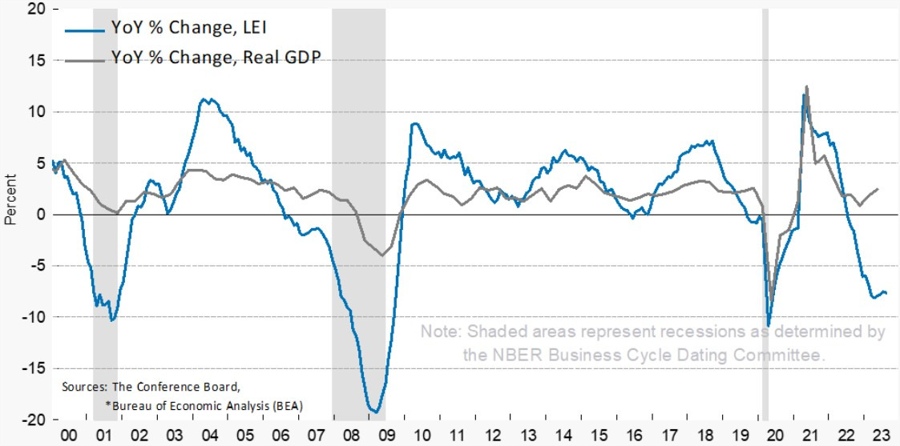

The US LEI Index declined by 0.4% in August following a 0.3% decline in July. The Leading Economic Index has now fallen for 17 straight months.

Friday:

ECB’s Lane (dove – voter) sees the monetary policy transmission firmly taking hold and expects rates to be held at 4% for sufficiently long:

- Sees staggered reset of prices and wages across the economy, a process which is ongoing.

- Dynamics of wages and profits in the coming quarters still an open question.

- The transmission of our monetary policy to broader financing conditions and the real economy is firmly taking hold.

- Central banks try to hit inflation in the medium term.

- Inflation over 2% is costly for the economy.

- Says won't be speculating on future European Central Bank policy moves.

- The most efficient wat to tighten monetary policy is via interest rates.

4% rate will do quite a bit to bring inflation to 2%.

ECB is still very data dependent.

Expect rates to held sufficiently long at 4%.

Key wage data will not be available until sometime in the 2024.

Not seeing a toxic mix that will trigger a recession.

The Australian Manufacturing PMI fell further into contraction while the Services PMI jumped back into expansion:

- Manufacturing PMI 48.2 vs. 49.6 prior.

- Services PMI 50.5 vs. 47.8 prior.

The Japanese CPI data matched the prior readings with inflation remaining at cycle highs:

- Japan CPI Y/Y 3.2% vs. 3.3% prior.

- Japan Core CPI Y/Y 3.1% vs. 3.0% expected and 3.1% prior.

- Japan Core-core CPI Y/Y 4.3% vs. 4.3% prior.

The Japanese Manufacturing PMI fell further into contraction with the Services PMI remaining in expansion:

- Manufacturing PMI 48.6 vs. 49.6 prior.

- Services PMI 53.3 vs. 54.3 prior.

The BoJ kept its monetary policy unchanged as expected with the interest rate at -0.10%:

- Maintains 10-year JGB yield target around 0%.

- Maintains band around its 10-year JGB yield target at up and down 0.5% each.

- Maintains offer to buy 10-year JGB at 1.0% daily through fixed-rate market operations.

- Makes no change to forward guidance.

- Japan's economy recovering moderately.

- Japan's economy likely to continue moderate recovery.

- Inflation expectations showing renewed signs of accelerating.

- Must watch financial and forex market moves and impact on Japan's economic activity, prices.

Moving on to the press conference, BoJ Governor Ueda repeated that they are ready to ease more if necessary and that they are not yet sure that inflation can reach the 2% target sustainably:

- Will not hesitate to take additional easing measures if necessary.

- We are yet to foresee inflation reaching 2% in a stable manner.

- Japan economy is recovering moderately.

- Wages and price setting behaviour has been more positive recently.

- (Clarified on the recent interview where he mentioned a “quiet exit” from monetary easing) I said that we need to patiently continue easy policy.

- We could consider ending yield curve control and modify negative interest rate policy.

- But only when we judge that achievement of 2% inflation is in sight.

- We are not in a situation now to decide on the order of change in policy tools.

- One of the most important factors to judge prices is strength of wage growth.

The UK August Retail Sales missed expectations with some minor positive revisions to the prior readings:

- Retail Sales Y/Y -1.4% vs. -1.2% expected and -3.1% prior (revised from -3.2%).

- Retail Sales M/M 0.4% vs. 0.5% and -1.1% prior (revised from -1.2%).

- Core Retail Sales Y/Y -1.4% vs. -1.3% and -3.3% prior (revised from -3.4%).

- Core Retail Sales M/M 0.6% vs. 0.6% expected and -1.4% prior.

French PMIs missed expectations by a big margin falling deeper into contraction:

- Manufacturing PMI 43.6 vs. 46.0 expected and 46.0 prior.

- Services PMI 43.9 vs. 46.0 expected and 46.0 prior.

German PMIs beat expectations across the board:

- Manufacturing PMI 39.8 vs. 39.5 expected and 39.1 prior.

- Services PMI 49.8 vs. 47.2 expected and 47.3 prior.

The Eurozone Manufacturing PMI missed expectations while the Services PMI beat forecasts although they both remain in contraction:

- Manufacturing PMI 43.4 vs. 44.0 expected and 43.5 prior.

- Services PMI 48.4 vs. 47.7 expected and 47.9 prior.

The UK Services PMI fell further into contraction while the Manufacturing PMI saw a small bounce:

- Manufacturing PMI 44.2 vs. 43.0 expected and 43.0 prior.

- Services PMI 47.2 vs. 49.2 expected and 49.5 prior.

The Canadian July Retail Sales missed forecasts although the core reading was much better than expected:

- Retail Sales Y/Y 2.0% vs. -0.6% prior.

- Retail Sales M/M 0.3% vs. 0.4% expected and 0.1% prior.

- Core Retail Sales M/M 1.0% vs. 0.5% expected and -0.7% prior (revised from -0.8%).

- August advanced estimate -0.3%.

ECB’s de Cos (dove – non voter) joins the others in the higher for longer camp:

- Underlying inflation is now easing.

- Inflation seems to be turning a corner.

- Current interest rate level - if maintained for sufficiently long - is broadly consistent with achieving the target.

- Too early to talk about rate cuts.

- Would be cautious about discontinuing PEPP reinvestment.

- Selling bonds is not something the ECB is currently considering in the future.

The S&P Global US Manufacturing PMI beat expectations while the Services PMI missed:

- Manufacturing PMI 48.9 vs. 48.0 expected and 47.9 prior.

- Services PMI 50.2 vs. 50.6 expected and 50.5 prior.

Fed’s Collins (neutral – non voter) leans on the higher for longer stance acknowledging the current resilience in the economy:

- Optimistic inflation can fall with only a "modest" rise in unemployment, see a widened pathway to that outcome.

- Current policymaking requires "considerable" patience to get the right signal from data.

- Despite "encouraging" recent data, inflation remains too high.

- Key elements of inflation, such as core services excluding shelter, haven't demonstrated "sustained" improvement.

- Supports vigilance regarding inflation risks; believes it's "too soon to be confident" that inflation is under control given the continued above-trend economic activity.

- Cash levels are reverting to "pre-pandemic norms"; anticipates household and business spending to be more influenced by high interest rates.

- Some inflation readings have been encouraging.

- Economic activity continues to be above trend.

Fed’s Bowman (hawk – voter) expects further interest rates increases as the economy remains too strong for a timely achievement of their inflation goal:

- Further interest rate increases likely appropriate with inflation "still too high”.

- Fed policy will need to be held at a restrictive level "for some time" to return inflation to 2% "in a timely way."

- Continued risk of further increase in energy prices could reverse some of the recent progress on lowering inflation.

- Economy still growing at a "solid pace," with robust consumer spending and solid job gains.

- Bank lending standards have tightened but no sign of a "sharp contraction" of credit that would significantly slow the economy.

- Expect progress on inflation is "likely to be slow" under current conditions, suggesting the need for even tighter policy.

- It's imperative that bankers provide feedback on recent plans to toughen bank rules.

The highlights for next week will be:

- Monday: German IFO.

- Tuesday: US Consumer Confidence.

- Wednesday: BoJ Meeting Minutes, Australia Monthly CPI, US Durable Goods Orders.

- Thursday: Australia Retail Sales, US Q2 Final GDP, US Jobless Claims.

- Friday: Japan Tokyo CPI, Japan Unemployment Rate, Japan Retail Sales, UK Q2 Final GDP, Eurozone CPI, Canada GDP, US Core PCE.

That’s all folks, have a great weekend!