- Crude oil surges, settling at $71.58, marking a 3.04% increase

- Mexico central bank keeps rates unchanged at 11.25%

- Atlanta Fed GDPNow forecast leaps to 2.6% from 1.2%

- ECB sources:ECB policy members are united on forecasting rate cuts later than the market

- Big jump in the Atlanta Fed GDPNow to 2.6% from 1.2% last. Strong growth projected.

- Crude oil surges as traders find support, sparking potential upside

- Lagarde highlighted data dependency for rate cut outlook. The market sees 148 bps in cuts

- European equity close: The early glow fades

- US retail sales are decelerating with a further dip likely to come ahead - CIBC

- US October business inventories -0.1% vs 0.0% expected

- Kickstart your FX trading on Dec. 14 with a technical look at the EURUSD, USDJPY & GBPUSD

- Lagarde Q&A: We need to see more data on wages

- Canadian November home prices -1.1% m/m - CREA

- Lagarde opening statement: The risks to economic growth remain tilted to the downside

- US November import prices -0.4% vs -0.8% estimate

- US initial jobless claims 202K vs 220K estimate.

- US November retail sales +0.3% vs -0.1% expected

- Canada October manufacturing sales -2.8% vs -2.7% expected

- ECB leaves key interest rates unchanged in December monetary policy meeting

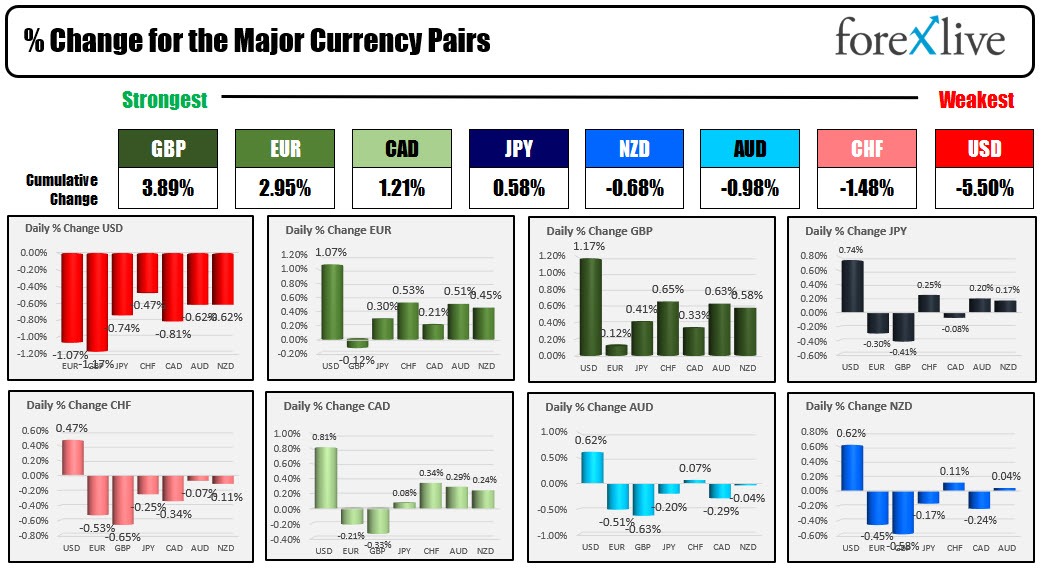

- The GBP is the strongest and the USD is the weakest as the NA session begins.

- BOE's Bailey: We cannot say that interest rates have peaked

- ForexLive European FX news wrap: Dollar extends post-FOMC slump, SNB and BOE on hold

- Pound gains as BOE offers no pivot, at least for now

- BOE leaves bank rate unchanged at 5.25% as expected

Day 2 of central bank decisions. Yesterday, the Fed and Chair Powell were more dovish, sending yields sharply lower. Today, the Swiss National Bank, the Bank of England, European Central Bank and later in the day, the Central Bank of Mexico, all weighed in with their recent rate decision. For each of them, they too kept rates unchanged. However, safe to say, the decisions were tilting more to the hawkish side.

The Bank of England highlights:

Vote Outcome: The Bank rate vote ended in a 6-3 decision, which was in line with expectations. Greene, Haskel, and Mann were the members who voted for a 25 basis points increase.

Decision Nuance: The choice between hiking rates or holding them was again a close call, indicating the complexity of the current economic situation.

Inflation Outlook: The Bank acknowledges that there is still significant progress to be made in reducing inflation and is committed to taking necessary actions to bring inflation back to the target of 2%.

Policy Stance: The Bank indicates that monetary policy will need to be restrictive enough, and for a long enough period, to effectively combat inflation.

Uncertainty Over Inflation Trends: Most policymakers are of the view that it's too early to assert that services inflation or pay growth are consistently decreasing.

Potential for Further Tightening: The Bank suggests that additional tightening of monetary policy may be necessary if persistent inflationary pressures are observed.

Inflation Forecast: The Bank now forecasts inflation to be just under 4.5% by the end of the year, slightly lower than the previous forecast of 4.75%

For the ECB, its highlights from the statement included:

ECB Interest Rates Unchanged: The key interest rates remain at 4.50%, 4.75%, and 4.00%.

Inflation Forecast: Expected to temporarily rise, then gradually decrease to the 2% target by 2025.

Economic Growth Outlook: Subdued in the short term, with growth projected at 0.6% in 2023, increasing to 1.5% by 2025 and 2026.

Policy Commitment: The ECB aims to maintain rates at levels that help achieve the 2% inflation target, with decisions based on economic data and inflation dynamics.

Balance Sheet Strategy: Continuation of reinvesting PEPP funds until mid-2024, then reducing the portfolio by €7.5 billion per month in the second half of 2024, ending reinvestments by year-end.

Refinancing and Asset Purchases: Ongoing assessment of refinancing operations' impact on monetary policy; gradual decline of the APP portfolio.

Readiness to Adjust Tools: The ECB is prepared to modify its instruments to maintain its 2% inflation target and ensure effective monetary policy transmission.

Below are the highlights in categories from Lagarde's press conference:

Inflation Trends and Expectations:

- Broad-based decline in inflation recently observed.

- Inflation expected to rise in December due to base effects, but a slow decline is anticipated afterwards.

- All measures of underlying inflation declined in October.

- Underlying inflation measures have risen due to wage growth and falling productivity.

- Longer-term inflation expectations are around the 2% target.

Economic Growth Risks:

- The risks to economic growth remain predominantly on the downside.

- Weak prospects are noted for the construction and manufacturing sectors.

- A softening is expected in the services sector.

ECB's Inflation Target:

- hello Strong determination to ensure inflation returns to the ECB's 2% target in the medium term.

Wage Data and Policy Decisions:

- Emphasis on the need for more data on wages, acknowledging that wage data is not declining.

- Decision-making in 2024 will be data-dependent to ascertain if the declining inflation trend is sustainable.

ECB's Monetary Policy:

- No discussions on rate cuts in the recent meeting.

- The decision on the Pandemic Emergency Purchase Programme (PEPP) was supported by a large majority, with varying opinions on the timing of tapering.

- Current forecasts indicate reaching a 2% inflation rate at the end of the projection period, with a slight overshoot to 2.1% anticipated by the end of 2025. These projections are based on data as of November 2023.

- The ECB will continue to evaluate their three criteria for monetary policy in the coming months.

The markets interpreted both central banks as being less dovish/more hawkish when compared to the Fed, and that led to increased USD selling vs the EUR and the GBP. Those two currencies are ending the day as the strongest of the major currencies, while the USD is the runaway weakest of the majors.

For the EURUSD, it moved up from 1.0874 close yesterday to a high just above the natural target level at 1.1000. The price tested the high from November 28 at 1.1008 and stalled just short of the November 29 high at 1.1016. Getting above those levels is needed to keep the bullish train moving in the new trading day (see video on the EURUSD here).

For the GBPUSD, it moved it move to it's highest level since August 2023 and in the process extended above the 61.8% of the 2023 range at 1.2719. That level will be close support into the new trading day. Staying above keeps the buyers firmly in control (see video on the GBPUSD here).

Looking at other markets today:

- Crude oil is trading up $2.15 or +3.08% at $71.61 and in the process reached up to test the November low at $72.37. The high reached $72.46 but stalled and rotated back down.

- Gold is trading up $8.22 or 0.42% at $2036. The price of gold reacted to lower rates and lower USD.

- Bitcoin is trading back at $43000 after opening slightly higher at $43,118

In the US debt market, the yields continued their move to the downside with the 10 year moving back below 4%. The US 10 year yield moved from a high on Monday at 4.29%. The low yield today reached 3.887%.

A snapshot of the market shows:

- 2-year yield 4.390%, -9.1 basis points

- 5 year yield 3.904%, -9.9 basis points

- 10-year yield 3.922%. -11.0 basis points.

- 30-year yield 4.042%, -14.2 basis points.

Finally, the US stocks closed higher for the 6tgh consecutive days. The Dow 30 and the small cap Russell 2000 were the biggest winners as the market rotate out of the big cap tech and into the less frothy small caps and industrials.

- Dow industrial average rose 158.11 or 0.43% at 37248.36

- S&P rose 12.46 points or 0.26% at 4719.54

- Nasdaq rose 27.58 points or 0.19% at 14761.55

- Russell 2000 surged 53 points or 2.72% at 2000.51.

Cathie Woods Ark Innovation increased $1.85 or 3.69% to $52.02.

Caterpillar, a proxy for capital-intensive industry, surged 6.42% to $285.17, its largest increase since August 1 when the price surged to new all time highs before starting a 23.8% decline to its October 31 lows. The all-time high price reached $293.88. The low at the end of October reached $223.76.