Monday:

Over the weekend Hamas launched a massive attack against Israel from Gaza which led to Israel to declare war against Hamas and invoking Article 40 Aleph for the first time since October 1973. The first reaction in the markets at the open was of risk aversion with equities lower, bonds higher, safe haven currencies higher and gold and crude oil higher. Most of the moves were faded soon after as the conflict is unlikely to change much the big picture as long as it doesn’t escalate to other Arab countries joining Hamas.

ECB’s Kazaks (hawk – voter), as other ECB members, is leaning towards a pause:

- The phase of rapid rate hikes is already behind us.

- Can currently count on the fact that we may pause.

- So, any future rate hikes would be relatively small.

ECB’s de Guindos (dove – voter) sees the current level of rates enough to bring inflation back to target:

- Inflation to fall in the coming months.

- But urges caution due to evolution of oil prices.

- Expects current level of interest rates to contribute to price stabilisation.

Fed’s Logan (hawk – voter), as other FOMC members, highlighted the rise in long-term yields as something that could do the job for the Fed without requiring additional rate hikes:

- Continued restrictive financial conditions will be necessary to bring down inflation.

- In setting policy rate, Fed must take account of financial conditions, which have tightened substantially in recent months.

- If higher long-term rates are due to higher term premiums, there may be less need for Fed to raise rates.

- Higher term premiums have clear role in higher long-term rates, uncertain how big.

- To the extent a stronger economy is behind rising long-term rates, Fed may need to do more.

- Attentive to wrists on both sides of Fed's mandate. High inflation is the most important risk.

- Progress on inflation encouraging but too early to be confident it is heading to Fed's 2% target in a sustainable, timely way.

- Labor market is still very strong, wage is still solid.

- Output and spending have been surprisingly strong, outlooks for consumer are mixed.

- There is a lot of uncertainty over the trade-off with the unemployment rate.

- It is important to stay focused on restoring price stability.

- The China slowdown is something to watch.

- Surprising strength of the economy creates risk for inflation. We have more work to do.

- Quite a bit of room for Fed balance sheet run off.

- Financial conditions tightening has been rapid but orderly.

- She has been thinking about how to square overall economy with Fed tightening so far.

- Tends to think that monetary policy lags are shorter than others.

- The bulk of economy is adjusting more quickly to monetary policy.

- Fed's focus and mine is the 2% inflation target.

- Looking at financial markets and performance of economy, the long-term neutral rate may be higher.

- Have seen tightening of bank lending standards, similar to what we expect and intend with policy tightening.

Fed’s Jefferson (neutral – voter) sounds cautious as the uncertainty around the economic outlook remains very high but leans towards a higher for longer stance:

- We need to move carefully to balance the risks of tightening too much or too little.

- May be too soon to say confidently we have tightened enough.

- Mindful of lag effects of past rates as I consider whether we will need further policy tightening.

- Rising long-term yields in the past may have meant investors seek stronger economic momentum and need for higher for longer Fed rate path.

- Mindful that changes in real yields can arise from changes of investors view of risk, uncertainty.

- Will keep higher bond yields in mind in assessing future rate path.

- Recent inflation data encouraging, but inflation still too high.

- Core PCE prices will moderate further as labour market comes into better balance.

- Labor market remains tight, but labour demand is falling. Supply is improving.

- There is a path to restoring price stability without a large gain in unemployment.

- Expect further gradual easing of labour market conditions.

- I am particularly attentive to upside inflation risks from a strong economy, labour market, energy prices.

- Downside risks to economic activity include slowdown in China, and Europe.

- It could be the case that rise in the long-run treasury yields reflects anticipation for strong growth.

- Current policy is restrictive.

- Finding the right stance of policy is my concern.

- As a policymaker I’m mindful cumulative effects of past rate increases has NOT been felt.

- We need to do our work to bring the inflation rate down before we can assess what long-run R-star is.

- Cannot say if rate cuts might be needed next year yet.

- Our objective is for balance sheet policy to work in harmony with policy rate, but it depends on what is happening in the economy.

- Need to be nimble with regard to what is happening in the economy.

- Employment growth is a good thing.

- We just want job growth to be consistent with path of inflation toward 2%.

BoE’s Mann (hawk – voter) stresses the risk of inflation expectations de-anchoring if inflation stays high for too long, which would require eventually an even more aggressive tightening and a worse recession:

- Says wage and price inflation are sticky downwards.

- Going forward the length of time inflation remains above target will be important given that inflation expectations tend to drift.

- Possible drift in expectations implies that policy has to be more aggressive.

- The longer inflation remains above target the more aggressive central bankers need to be in reacting to it.

- Policymakers need to address not just high inflation today but the risk of rising expectations in the future.

- Policy has to be more aggressive because it has to address both a drift in expectations as well as the actual inflation.

- From a risk management perspective, I am more concerned about this embeddedness, the duration, the expectations.

Tuesday:

ECB’s Villeroy (neutral – voter) continues to think that additional rate hikes are unlikely:

- At this stage, further rate hikes are not the right thing to do.

- Interest rates are on a good level.

- Events in Israel add to economic incertitude.

- Wary about oil price developments over Israel situation.

Kyodo News reported that the BoJ is mulling raising FY 2023/24 Core CPI target to 3.00% vs. 2.5% forecast in July. This is a signal that they do see high core inflation persisting, but they keep on highlighting that wage growth is what is needed for them to achieve their inflation target in a sustainable way.

Bloomberg reported that China is weighing new stimulus and higher deficit for spending on infrastructure to meet the growth target and bolster the economy.

The US September NFIB Small Business Optimism Index came in lower than expected at 90.8 vs. 91.0 expected and 91.3 prior.

Details:

- Plan to Hire 18 vs. 17 prior.

- Higher selling prices 29 vs. 27 prior.

- Positions not able to fill 43 vs. 40 prior.

- Net compensation plans 23 vs. 26 prior.

Fed’s Bostic (dove – non voter) doesn't see the need for additional rate hikes:

- Inflation has improved considerably, still a long way to go.

- We're in a good place for us to get to 2% inflation.

- There's certainly more for us to do.

- I don't have a recession in my dot plot.

- We don't have to increase rates any further.

- If things come in differently from my outlook, we might have to increase rates but that's not my current outlook.

Below the results from the NY Fed Consumer Inflation Expectations survey:

- Year-ahead inflation 3.7% vs. 3.6% prior.

- Three-year inflation 3.0% vs. 2.8% prior.

- Five-year inflation 2.8% vs. 3.0% prior.

- Median home price rise 3.0% vs. 3.1% prior.

- Credit access perceptions weakened in September.

Fed’s Kashkari (hawk – voter) is another member highlighting the rise in long term yields and how that is likely to do the job for the Fed:

- Inflation is headed down.

- I'm optimistic we can shrink the Fed's balance sheet back to pre-crisis trend line.

- We are seeing higher long-term Treasury yields but not higher inflation.

- Reason for rise now in 10-year yield is a bit perplexing; one story is it is higher growth expectations.

- It's possible that higher bond yields could leave less for the Fed to do.

- If higher long-term yields are due to expectations about Fed actions, we may need to deliver.

- We will need to look at wage and inflation data for me to get comfortable we've done enough.

Fed’s Daly (neutral – non voter), as the other FOMC members, acknowledged that the higher long term yields could be the equivalent of another rate hike and thus be the reason for another pause at the November FOMC meeting:

- Decline in goods inflation has been an easy win, and not largely due to the Fed's rate hikes.

- Just starting to see improvement in non-housing services inflation, need more of it.

- We have more work to do, inflation is still high.

- Fed policy is helping supply and demand get into a better balance.

- In future could see the nominal neutral rate go to 2.5%-3.0%.

- The new normal may be a little different, but probably won't be a gigantic reset.

- I don't manage markets, I watch them for information.

- If bond yields are tight, that could be the equivalent of another rate hike.

- The risks to the economy are more balanced.

- We need to get inflation down to fully balance the economy.

Wednesday:

RBA’s Kent highlights the slowdown in growth and inflation due to restrictive monetary policy and that the lags mean that further effects will be felt in the near future:

- Monetary policy is slowing the growth of demand, inflation.

- Policy lags mean some further effects of past rate hikes are still to be felt through the economy.

- Repeats that some further tightening of policy may be required to ensure inflation slows.

- The effect of slower demand growth on inflation is now building.

- Hearing in liaison that a range of retailers discounting in the face of weak consumer spending.

- Mortgage payments are at a record share of household disposable income, will rise further.

- The rise in interest rates has also increased incentives to save.

- Board is paying close attention to economic developments here and overseas.

- Have the opportunity to see how economy reacts to past hikes.

- No current plans to step up the pace of bond holdings.

- If we were to sell bonds, would do it in a way that would not disturb markets.

- There are pockets of fast wage growth but contained in aggregate.

- The CPI data will be important, but it is not the only consideration for policy.

Fed’s Bowman (hawk – voter) continues to support another rate hike as she doesn’t like the tightness in the labour market:

- Interest rates may need to rise further.

- Inflation remains well above the FOMC's 2% target.

- Job market remains tight.

- This suggests policy rate may need to rise further.

- And stay restrictive for some time to return inflation back to target goal.

ECB’s Knot (hawk – voter) is comfortable with the current level of rates but stands ready to adjust if the disinflationary process stalls:

- Policy is in a good place now.

- Inflation is still too high.

- But effects of inflation shock are waning.

- Economic cooldown desirable to tame inflation.

- Restrictive policy will be needed for some time.

- Stands ready to adjust rates further if disinflation process stalls.

ECB’s de Cos (dove – non voter) is on the higher for longer camp:

- Core inflation has turned a corner.

- More confident that inflation trajectory might lead us to 2% target.

- If rates are maintained for a sufficiently long period, we could get there.

- Market has understood very well our communication.

- Growth risks skewed to the downside.

- It is premature to discuss rate cuts.

The September US PPI beat expectations across the board:

- PPI Y/Y 2.2% vs. 1.6% expected and 2.0% prior (revised from 1.6%).

- PPI M/M 0.5% vs. 0.3% expected and 0.7% prior.

- Core PPI Y/Y 2.7% vs. 2.3% expected and 2.5% prior (revised from 2.2%).

- Core PPI M/M 0.3% vs. 0.2% expected and 0.2% prior.

Fed’s Waller (hawk – voter) is another member citing higher yields as a reason to hold rates steady at the November meeting:

- We will see how higher long-term rates feed into Fed policy.

- The real side of the economy is doing well.

- If current trends continue, inflation will basically be back to target.

- Fed can watch and see what happens on rates.

- Clearly, issuance has to have an impact on yields.

- When the deficit is 6% with low unemployment, it's unsustainable.

- Now, once again, financial markets are tightening up. They're going to do some of the work for us.

ECB’s Kazaks (hawk – voter) didn’t add much to his prior comments as he leans towards a pause:

- The door on rate hikes cannot be closed.

- Interest rates are currently appropriate to get inflation to 2% in H2 2025 but door on rate hikes can't be closed.

- Talks on mandatory higher reserve requirements for banks are appropriate.

- Italian spreads not unwarranted and not worrisome.

The Fed released the FOMC Minutes of its September Monetary Policy Meeting:

- Participants judged that risks had become more two-sided.

- Many participants saw downside risks to economic activity and upside risks to the unemployment rate.

- Vast majority of participants judged future path of economy as highly uncertain.

- More evidence needed to be confident price pressures ebbing.

- Several participants commented that, with the policy rate likely at or near its peak, the focus of monetary policy decisions and communications should shift from how high to raise the policy rate to how long to hold the policy rate at restrictive levels.

- Participants stressed that current inflation remained unacceptably high while acknowledging that it had moderated somewhat over the past year.

- All participants agreed that policy should remain restrictive for some time until the Committee is confident that inflation is moving down sustainably toward its objective.

- Several participants noted that the process of balance sheet runoff could continue for some time, even after the Committee begins to reduce the target range for the federal funds rate.

- The economic forecast prepared by the staff for the September FOMC meeting was stronger than the July projection, as consumer and business spending appeared to be more resilient to tight financial conditions than previously expected.

- The staff assumed that GDP growth for the rest of this year would be damped a bit by the autoworkers' strike, with these effects unwound by a small boost to GDP growth next year. The size and timing of these effects were highly uncertain.

Fed’s Collins (neutral – non voter) is leaning towards another pause in November and besides cooler core inflation wants also to see a softer labour market:

- Fed is at or near peak of rate hike cycle.

- Further rate hike could be warranted depending on incoming data.

- Expects Fed to keep policy restrictive for some time.

- Policy must stay restrictive until clear sign inflation moves to target of 2%.

- Optimistic inflation can be tamed with ‘orderly slowdown,’ small jobless rise.

- Policy patience will give Fed time to get read on economy.

- Main uncertainty is measuring impact of past Fed actions.

- Fed faces challenges in extracting signal from economic data.

- Cooler core inflation will need softer labour market.

- Too soon to say core inflation on trend for 2%.

- Chance of a soft landing has gotten higher for economy.

- As savings dwindle, economy becoming more responsive to rate policy.

- Federal Reserve will factor in 'unrest in the Middle East'.

- Economy has yet to feel the full impact of FOMC rate hike cycle.

- Sees no reason to change the Fed's inflation target.

RBNZ Governor Orr just stated the obvious and keeps supporting the central bank’s “wait and see” stance:

- Official Cash Rate (OCR) from 2% to 5.5% was the most rapid increase in the Reserve Bank’s history. The effects of this are flowing through as anticipated to our economy.

- OCR will need to stay at restrictive levels for the foreseeable future to ensure annual consumer price inflation returns to our 1% to 3% target range, while supporting maximum sustainable employment.

Thursday:

ECB’s Vujcic (hawk – voter) is comfortable with the current level of interest rates and seems inclined to wait at least until early 2024 before deciding on what to do next:

- Too soon to declare victory over inflation.

- Early 2024 data will bring more clarity on wages, which will provide officials with an improved but not necessarily definitive view of consumer price inflation.

- I wouldn’t think that December is when we will be able to say mission accomplished, we have to be more patient.

- More interesting for me will be to see how the data come in in spring of next year, when we’ll have more clarity on labour-market pressures, and particularly wage-growth developments.

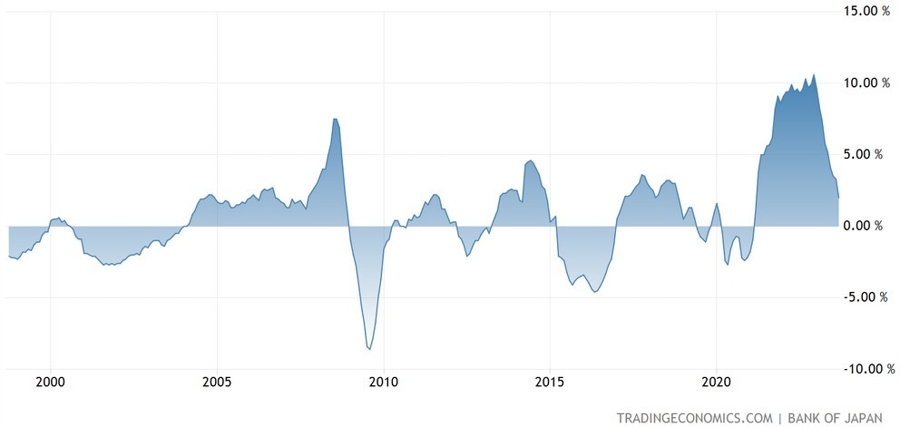

The Japanese September PPI missed expectations:

- PPI Y/Y 2.0% vs. 2.3% expected and 3.2% prior.

- PPI M/M -0.3% vs. 0.1% expected and 0.3% prior.

BoJ’s Noguchi, as other BoJ members, is focusing on wage growth as a crucial factor to exit their easy monetary policy:

- Biggest focus is whether wage hike momentum will be maintained or not.

- Raising of YCC allowance band does not signify a tightening of monetary policy.

- If central banks hold rate hikes and inflation comes down, the risk of hard landing will be reduced.

- Japan's economy is recovering gradually.

- When inflation expectations are in a stage of rising, some flexibility is needed to continue easy policy under YCC.

- Chinese economy facing risk of deflation or 'Japanisation'.

- Need to pay close attention to fiscal, monetary policy response to low inflation by Chinese authorities from now on.

- There are signs of upward price pressures coming down.

- BOJ's near-term mission is to realise a situation where wage growth does not fall short of inflation as soon as possible through persistent monetary easing.

- The trend of passing on costs for raw materials is widely continuing.

- Japan needs to shake off the 'zero norm' of prices and wages in order for nominal wage increase to exceed 2% as a trend.

- 3% nominal wage growth would correspond with 2% inflation target.

- We have no choice but to raise inflation forecast for fiscal year 2023.

- Inflation of this extent was unexpected.

- Growth rates and inflation both deviating upwardly.

- But inflation expectation does not factor in achievement of 2% inflation target.

The UK August Monthly GDP comes in line with expectations:

- GDP M/M 0.2% vs. 0.2% expected and -0.6% prior (revised from -0.5%).

- GDP Y/Y 0.5% vs. 0.5% expected and 0.3% prior (revised from 0.0%).

ECB’s Stournaras (dove – non voter) would like to see bond buying continue to keep flexibility around these uncertain times:

- Should not stop bond buying too early.

- No value in bringing forward end of PEPP.

- Now especially that there is new uncertainty from events in Israel and Palestine.

- Need to keep flexibility and act if necessary.

ECB’s Villeroy (hawk – voter) is just another member in favour of a higher for longer stance from now on:

- Current level of interest rates is appropriate.

- Patience is more important than activism at present.

- Duration is more important than level of interest rates.

BoE’s Pill (neutral – voter) is leaning on the higher for longer stance:

- It is a finely balanced issue if we still have to do more on rates.

- UK inflation remains too high.

- A lot of policy tightening has yet to come through.

The ECB released the Monetary Policy Accounts of its September meeting:

- Solid majority expressed support for 25 bps rate hike in September.

- Emphasis was also paced on upward revisions to headline inflation projections.

- A pause would have given rise to speculation that tightening cycle was over.

- Not hiking could also send a signal of ECB being more concerned about the economy than inflation.

- Deposit facility rate around 3.75% to 4.00%, as long as it was understood as being maintained for a sufficiently long duration, should be consistent to return inflation to target.

- Decision between rate hike and pausing was a close call but tactical considerations played a role as well.

The US CPI beat expectations on the headline figures, but the core measures were in line with forecasts:

- CPI Y/Y 3.7% vs. 3.6% expected and 3.7% prior.

- CPI M/M 0.4% vs. 0.3% expected and 0.6% prior.

- Core CPI Y/Y 4.1% vs. 4.1% expected and 4.3% prior.

- Core CPI M/M 0.3% vs. 0.3% expected and 0.3% prior.

- Core Services ex-Housing M/M 0.6% vs. 0.5% prior.

- Real weekly earnings -0.2% vs. -0.1% prior.

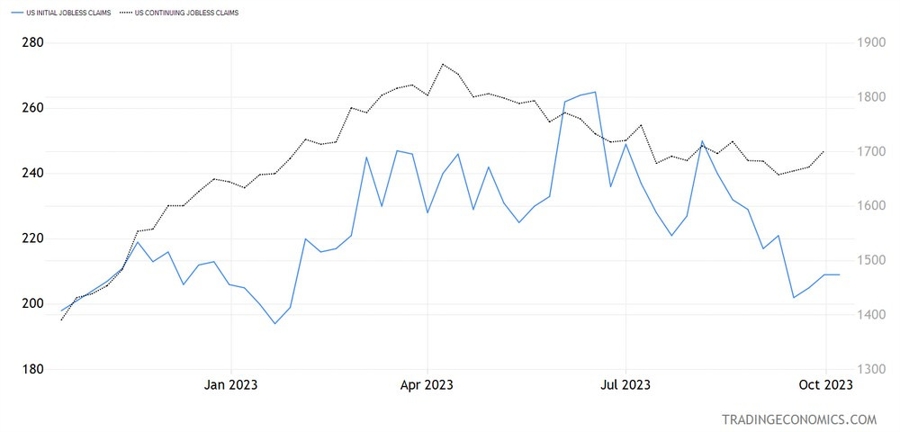

The US Initial Claims beat expectations once again, but Continuing Claims missed:

- Initial Claims 209K vs. 210K expected and 209K prior (revised from 207K).

- Continuing Claims 1702K vs. 1680K expected and 1672K prior (revised from 1664K).

Fed’s Collins (neutral – non voter) repeats that the rise in bond yields is likely to translate in another pause at the November FOMC meeting as the Fed wants to see even more data before proceeding with another rate hike:

- Fed is at or near the peak in rate hiking cycle.

- Too soon to take prospect of additional hike off the table.

- Bond yield rise likely reduces need for near-term Fed hike.

- Latest CPI underscores uneven progress towards 2%.

- Current monetary policy phase calls for patience.

- Too soon to say inflation on sustainable path towards 2%.

- Sees only limited progress on lower core services ex-housing inflation.

- Sees evidence the labour market is rebalancing.

- Resilient economy is why rates will need to say higher for longer.

- Is carefully watching commercial real estate, not seeing major trouble so far.

- Fed has not decided whether it will extend life of bank term funding program.

Friday:

A U.N. spokesman said that Israel’s military on Friday directed the evacuation of northern Gaza within 24 hours. This might be a signal of an impending ground offensive, although Israeli military has not yet confirmed the appeal.

The New Zealand Manufacturing PMI fell further into contraction:

- 45.3 vs. 46.1 prior.

The Chinese Inflation data missed expectations across the board:

- CPI Y/Y 0.0% vs. 0.2% expected and 0.1% prior.

- CPI M/M 0.2% vs. 0.3% expected and 0.3% prior.

- PPI Y/Y -2.5% vs. -2.4% expected and -3.0% prior.

The Chinese trade data was better than the previous figures, but still in negative territory:

- Exports Y/Y -6.2% vs. -7.6% expected and -8.8% prior.

- Imports Y/Y -6.2% vs. -6.0% expected and -7.3% prior.

BoE’s Bailey (neutral – voter) highlights the division among the MPC on policy outlook:

- Last policy decision was a tight one.

- Future decisions will continue being tight.

- Policy is restrictive and it has to be.

- Sees progress on inflation but there is still work left to do.

Fed’s Harker (neutral – voter) is in the higher for longer camp now:

- Fed is likely to be done with rate hikes.

- Supports higher-for-longer interest rate stance.

- Can't say for low long rates will need to remain high.

- Sees steadily disinflation, falling below 3% this year.

- Growth to moderate next year but he doesn't see a recession.

- Does not expect to see mass layoffs.

- Auto strikes and renewed student loan payments will weigh on economy.

- Expects unemployment rate to rise to about 4%.

ECB President Lagarde (neutral – voter) leans on the higher for longer stance as she’s counting on monetary policy lags to return inflation to their 2% target :

- We will return inflation to 2%, it is happening.

- There is more policy lag in the pipeline from past hikes.

The University of Michigan Consumer Sentiment survey missed forecasts by a big margin across the board with inflation expectations seeing a jump back up:

- Consumer Sentiment 63.0 vs. 67.2 expected and 68.1 prior.

- Current conditions 66.7 vs. 70.4 expected and 71.4 prior.

- Expectations 60.7 vs. 65.5 expected and 66.0 prior.

- 1-year inflation 3.8% vs. 3.2% prior.

- 5-10 year inflation 3.0% vs. 2.8% prior.

BoC Governor Macklem sounds hawkish as underlying inflation has been surprising to the upside and wage growth has been solid:

- Higher long-term bond yields are not a substitute for what needs to be done to get inflation back down to target.

- We are seeing clear signs monetary policy is working to rebalance supply and demand, but inflation is still too high.

- We're not really seeing downward momentum in underlying inflation and that is a concern.

- Strength of Canadian economy means people are getting wage increases that will help make it easier to digest impact of higher mortgage rates after renewal.

The highlights for next week will be:

- Monday: Japan Industrial Production, NZ CPI, PBoC MLF.

- Tuesday: RBA Meeting Minutes, UK Jobs report, German ZEW, Canada CPI, US Retail Sales, US Manufacturing Production, US NAHB Housing Market Index.

- Wednesday: China GDP, China Industrial Production, China Retail Sales, China Unemployment Rate, UK CPI and PPI, US Housing Starts and Building Permits.

- Thursday: Australia Jobs report, US Jobless Claims, Fed Chair Powell speaks.

- Friday: Japan CPI, PBoC LPR, UK Retail Sales, Canada Retail Sales.

That’s all folks. Have a great weekend!