What is a straddle?

A straddle means two transactions sharing the security, including positions offsetting one another. One of the operations is responsible for extended risk, the other for short. As a consequence, it involves the buying or selling of option derivatives that give the holder access to profit according to the moves in the price of the underlying security, with no regard to the direction of price change. The buying of particular option derivatives is called a long straddle, and the selling of the option derivatives is referred to as a short straddle.

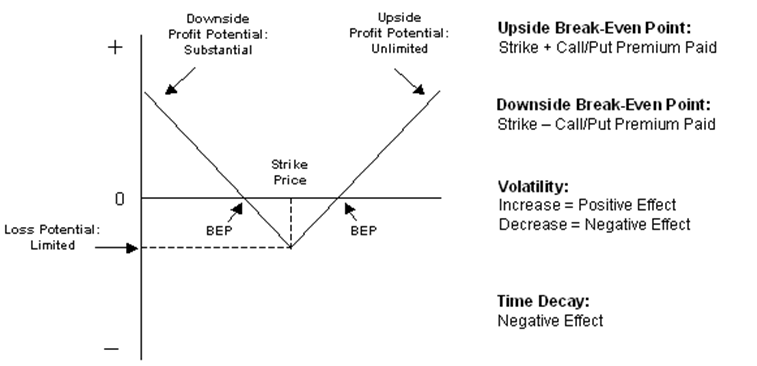

A long straddle usually includes buying both a call option and a put option on particular stock, index or interest rate. These two options are purchased at the identical strike price and have an expiration in the same period. The holder of a long straddle has his profit if the subjacent price changes significantly from the amount of purchase in any direction. So an investor can choose a long straddle position believing the market is volatile but is not sure about the guidance of this change. Helping him to limit risk because the biggest possible loss for the holder is the cost of these options. On the other hand, there are tremendous opportunities for profit.

For instance, company A is going to publish its quarterly financial data in two weeks. A trader thinks that these financial results will probably cause a significant change in company A's stock price, but not sure if the price will increase or decrease. He can choose a long straddle, where he receives profit regardless how the price of A stock changes if the price moves in any of directions. In case the price increases enough, he will take the call option and not the put option. If the price declines, he chooses the put option. If the price variation is not enough, he will have losses, with the high limit of the price of these two options. The risk is restricted to the total value paid for the options, in contrary to the short straddle in which the risk is almost unrestricted.

If the stock is volatile enough and the option has a long duration, the trader can have profited from two options. Forcing the stock change lower than the put option's strike price and higher than the call option's strike price in different periods of time before the option expires.

A short straddle means a strategy of binary options trading without direction that includes at the same time sale of a call and a put of the identical underlying security, expiration period and strike price. The earnings are restricted with the premium from the selling of call and put. The risk is not limited to significant changes in the price of underlying security upwards or downwards will make losses correlated to the volatility of the price change. The highest profit after expiration will be in case the underlying security is sold at the straddle's strike price. Then puts and calls involving the straddle lapses valueless letting straddle holder to have full credit obtained as their benefit. This approach is known as 'non-directional' strategy as the short straddle brings profit in case the underlying security slightly moves in price before the straddle's expiration.

A risk for the short straddle's owner position isn't limited because of the selling of the put and the call options that subject the investor to unrestricted possible losses (for the call) or losses restricted to the strike price (for the put), while the highest possible profit is the premium received by the primary selling of the options.

A tax straddle means used for taxes, usually applicable to futures and options to form a tax shelter.