Ahead of Thursday's ECB meeting, our call has not substantially changed from four weeks ago. Our

baseline is that the ECB will cut the depo rate by 10bp-tiering the

deposit rate would allow the ECB to do a small cut rather than a big

one. We think the focus will need to be on QE, which we expect to be

extended until September 2017 and accelerated by €10bn/month. We also

expect the ECB to make QE more credible-reserving the right to go even

further in the future-by tweaking the technical configuration.We think moving away from the capital key-which in our view would be

the ideal option-remains politically controversial and would push the

holding threshold beyond 33%. Buying below the deposit rate is the most

technically elegant and least politically sensitive solution and is thus

our baseline. We reiterate our view that this should be accompanied by a

commitment to maintain the average maturity close to the current level.

FX: EUR risks tilted to downside, but not sustained Our

economists' baseline scenario for the ECB is unlikely to be a

game-changer for the EUR. We believe buying more safe assets for longer

will not support the market's risk appetite, and banks have not been

eager to borrow from the TLTRO so far. These policies could have a

temporary market impact, but we do not see how they could offset the

implications of global risk aversion for Eurozone markets, or the

investors' concerns about the European banks. Still, we see the very short-term risks for the EUR as titled to the downside from the ECB meeting. We

would expect Draghi to use a very dovish tone and strengthen forward

guidance to argue that the ECB is willing to do whatever it takes to

reach its inflation target. We would also expect him to try his best to

weaken the Euro that day, to avoid a second disappointment after easing

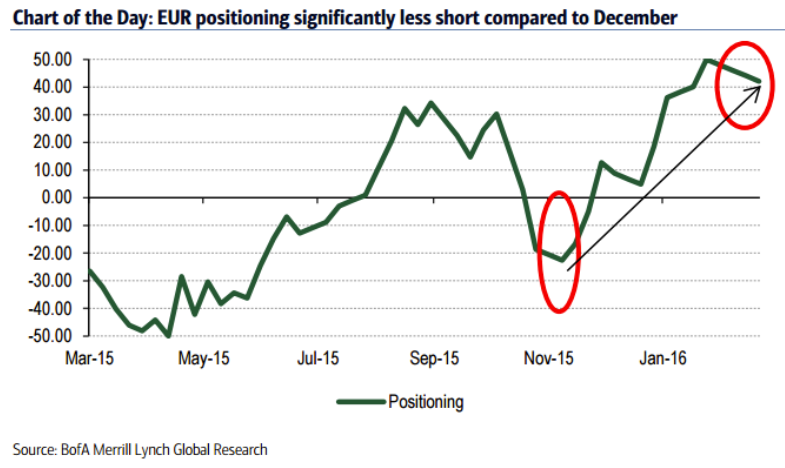

policies again. Positioning helps, with the market nowhere near the

stretched short EUR position of last December. Indeed, our last FX Vol

Trader report has recommended a EURUSD 3m 1.00 digital put as a high

risk-reward trade if the ECB exceeds modest market expectations. However, if the Euro does weaken on Thursday, we would be tactical and likely take profits soon. We

have argued that global factors are at this point a stronger driver for

FX than domestic monetary policies, as the BoJ discovered in January.

Post ECB, we see the US data and global market sentiment as the main EUR

drivers. In our view, sustained EUR weakness needs the Fed to continue

hiking rates, in addition to more ECB easing, and stronger global risk

appetite.