Societe Generale's FX Quant Fund which runs systematic currency strategies by SocGen's quant analysts.

The SG FX Enhanced Risk Premia strategy has continued to keep a

long dollar position during the week and has also increased the long

position in the EUR and the short allocation to highbeta G10 currencies.

The biggest longs are the USD, the EUR and the JPY. The most sizeable

shorts are the NOK, the NZD and the AUD. The long positions on GBP/USD

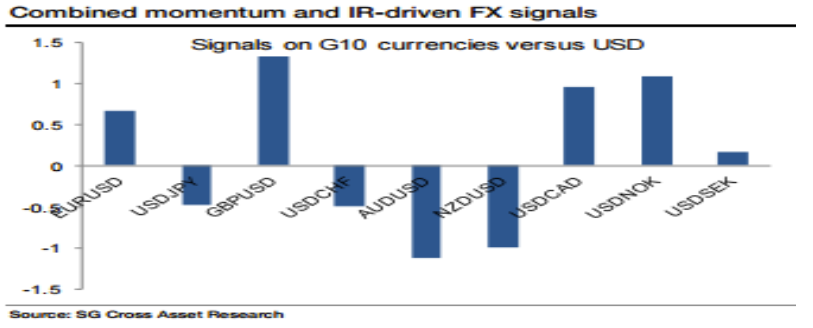

and USD/NOK and the short positions on AUD/USD and NZD/USD are the USD

crosses with the strongest combined momentum and IR-driven FX signals.

The static SG Sentiment indicator remains in the risk-averse area.

Based on the adaptive (tailored) version of the sentiment indicators and

the relevant time-series signals, we maintain a prudent approach

towards FX carry strategies: we have a long exposure to the Asia carry

basket and short exposures to the G10 and CEEMEA&LATAM carry

baskets.

The risk of the aggregate strategy remained conservative and stands

slightly above 7% annualised volatility. The strategy has been

profitable during the week at +2.7%, while the return for the month of

August so far has been sizeable at +3.4%.