The data agenda focus is on PMI reports from China for November. These are the official PMIs from the National Bureau of Statistics. The privately surveyed, and thus unofficial, PMIs from Markit/Caixin will follow later this week. These are different surveys, there is a greater representation of large and SEO firms in the official PMIs.

Factory activity is expected to have contracted further in these November figures. COVID restrictions hit production and exports fell. Chinese authorities did provide further stimulus. Last week the PBOC announced a cut to reserve requirements, which should free up cash for lending, but when folks are shut up inside activity, and demand for loans, suffers. There were also measures announced, a 16-point plan, to prop up the troubled property sector. Coronavirus restrictions were eased but were soon cranked back to extremely restrictive as the latest outbreak spread.

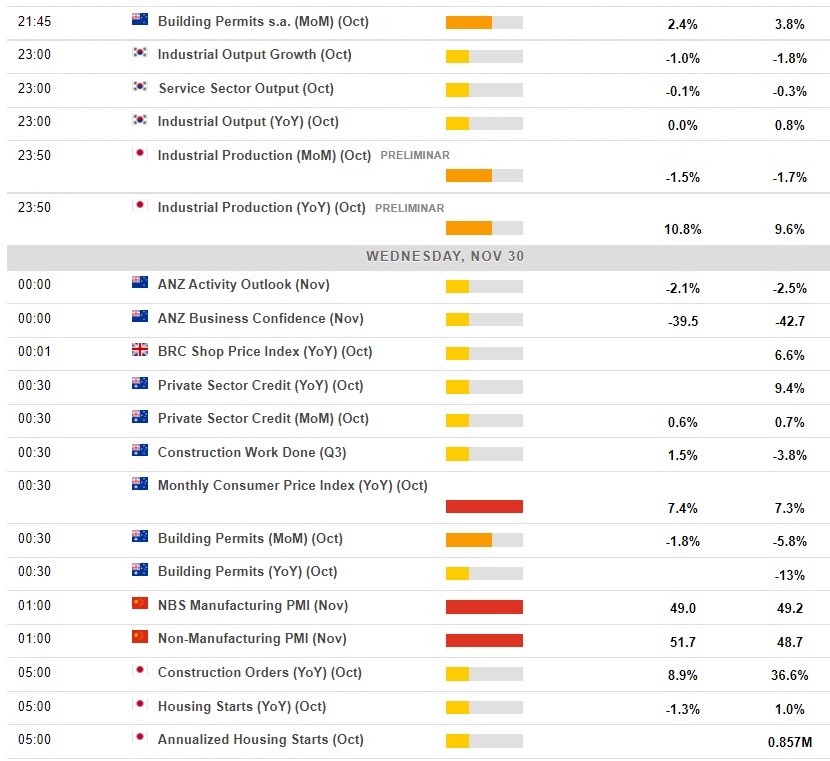

You can see the Manufacturing PMI is expected to have slipped further into contraction in the calendar snapshot below. On the services 'expected', I'd suggest the 51.7 is super-optimistic and a contractionary reading not far from October's level is more realistic.

Also on the agenda:

- Data from New Zealand at 2145 GMT at 0000 GMT.

- Data from Australia at 0030 GMT.

- This snapshot from the ForexLive economic data calendar, access it here.

- The times in the left-most column are GMT.

- The numbers in the right-most column are the 'prior' (previous month/quarter as the case may be) result. The number in the column next to that, where there is a number, is the consensus median expected.