- Prior 47.8

- Manufacturing PMI 43.8 vs 43.4 expected

- Prior 43.1

- Composite PMI 47.1 vs 46.9 expected

- Prior 46.5

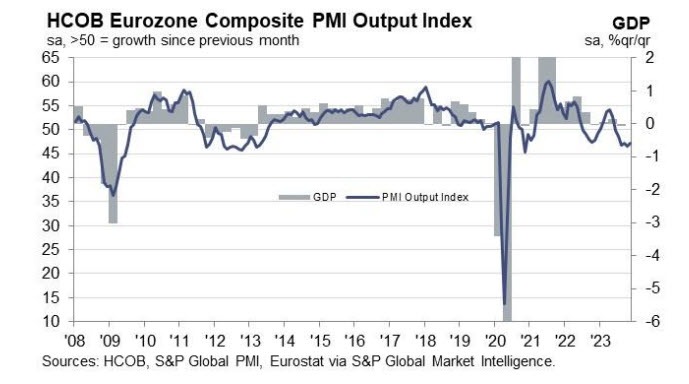

There are improvements across all sectors but the euro area economy continues to contract in November, albeit at a slower pace. That being said, employment conditions declined for the first time in almost three years and that is a concerning detail that the economic slowdown is starting to hit the labour market. Besides that, services inflation continue to be an issue as prices tick higher while manufacturing inflation remains in decline at least. HCOB notes that:

“The Eurozone economy is stuck in the mud. Over the last four to five months, the manufacturing and services sectors have both been experiencing a relatively constant contraction pace. Considering the flash PMI numbers for November in our nowcast model indicates the potential for a second consecutive quarter of shrinking GDP. This would align with the commonly accepted criterion for a technical recession.

“This is certainly not what the ECB likes to see. Despite the prevailing economic weakness, service providers continue to forge ahead with faster price increases in November, propelled by the astonishingly rapid and even accelerating increase in input costs. The latter can be mostly attributed to above average increases in wages, which play a major role in the services sector.

“The economic weakness, initially impacting industrial workers' jobs by mid-2023, is now poised to reach the services sector jobs market. Employment growth in this domain has nearly come to a standstill. Anticipating a continued downward trend for the next few months, there is a possibility of an uptick in the unemployment rate, which has shown resilience thus far.

“Looking for positive news, the spotlight falls on new orders. While they continue to contract at a brisk pace, the latest decline was the softest in four months. Coupled with a modestly improved outlook for manufacturing activity in the next 12 months, one might find rays of hope gleaming on the horizon for the coming year.

“The top two economies of the Eurozone find themselves in the grip of considerable weakness, with a slight advantage favouring Germany in November. Signs of improvement emerge as the composite index in Germany increased, contrasting with a weakening trend in France. However, challenges loom for Germany as it struggles to deliver on public investments, following the constitutional court's insistence on complying with the debt brake, potentially relegating Germany to the back seat in 2024.”