- A nasty close for the US stocks

- Economic calendar in Asia for Thursday, 17 August 2023 -

- Crude futures settle at $79.38

- Summary of FOMC meeting: Most thought inflation risks could require additional rate hikes

- Atlantic hurricane season may finally be getting underway

- European equity close: Italian stocks lag

- Atlanta Fed Q3 GDPNow tracker raised to a sizzling 5.8% from 5.0%

- PBOC-backed paper: Recent yuan fluctuations are normal

- EIA US weekly oil inventories -5960K vs -2320K expected

- July US industrial production +1.0% vs +0.3% expected

- Kickstart your trading day w/ a technical review/overview of the EURUSD, USDJPY and GBPUSD

- Target: US comp trends softened in late-May and June before a meaningful recovery in July

- Canada wholesale trade for June -2.8% versus -4.2% expected

- US July housing starts 1.452m vs 1.448m expected

- Canada July housing starts 255K vs 240K expected

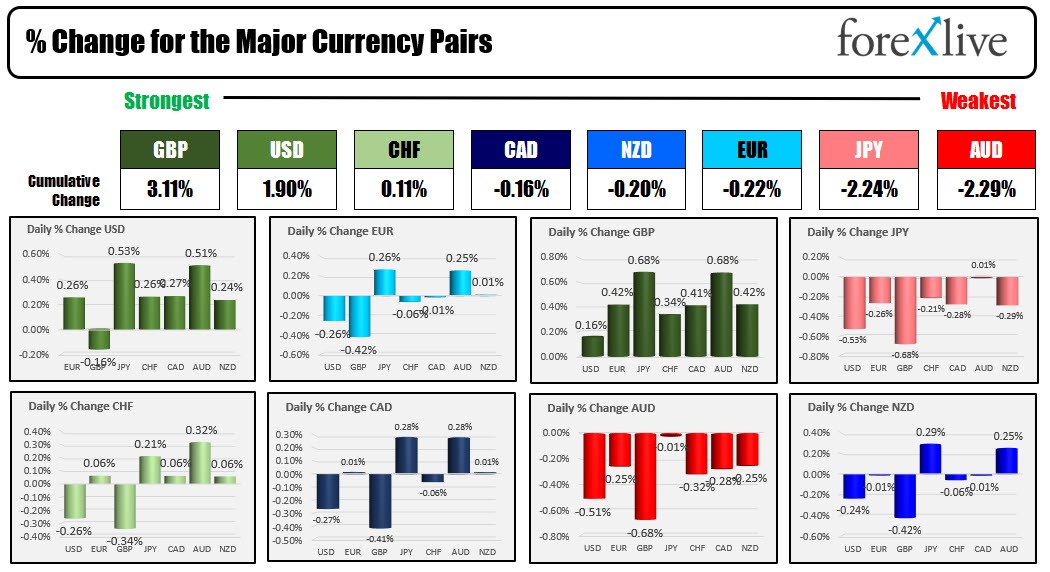

- The GBP is the strongest and the CHF is the weakest as the NA session begins

- ForexLive European FX news wrap: Pound gains on CPI data, risk mood more tentative

The GBP was the strongest of the major currencies after higher-than-expected CPI data was released in the UK session. The AUD was the weakest.

The USD moved higher today and just below the GBP for the strongest of the major indices. The dollar index (DXY) moved to the highest level since July 6 (see chart below). The high for the index moved to 103.52. The next target comes against the July 6 high at 103.572. Technically, the price closed above its 200-day moving average for the 1st time since November 30, 2022. Bullish for the DXY.

Helping the USD's run to the upside today was housing starts which were marginally higher than expectations, and industrial production which rose by 1% well above the 0.3% gain expected. Capacity utilization also was better-than-expected at 79.3% versus 79.1% expected (and 78.6% last).

The minutes from the July meeting said many thought it would take below-trend growth to bring supply and demand back in balance. The retail sales and data yesterday showed demand still is strong. The minutes also said that with inflation was still too high, and it would likely require more rate hikes.

The Atlanta Fed GDPNow model also continued its run to the upside with the 3Q growth currently modeling at 5.8% up from 5.0% yesterday. Admittedly the model estimates can fall sharply as new data points are released as the quarter progresses. Nevertheless, it is getting the market's attention and helping to push the greenback to the upside.

US yields are closing near highs for the day with the:

- 2-year yield at 4.978%, up 2.4 basis points

- 5-year yield 4.406% up 2.8 basis points

- 10-year yield 4.256% up 3.5 basis points

- 30-year yield 4.356% up 3.8 basis points

The 10-year yield moved to the highest level since October 2022. The high yield in 2022 reached 4.335%. The 30-year yield traded to a high of 4.377% which was just short of the high from yesterday 4.389%.

The USD moved the most vs the JPY with a gain of 0.53%. Technically the move higher took the USDJPY price to the highest level since November 10. In doing so the price also moved above a swing area between 144.984 and 145.90. Looking at the daily chart below, the next target comes against the upward-sloping trendline connecting 2023 highs. That level comes in at 147.80.

The AUDUSD was another big mover with the AUDUSD falling -0.51% (USD higher). That pair moved below the May 2023 low at 0.64587 and extended lower to 0.64157. The May 2023 low is now close risk. Stay below and the sellers are more in control. Looking at the daily chart below, the next target comes at 016348 – 0.6363 area. A downward-sloping trendline also cuts across within that swing area.

A snapshot around other markets shows:

- Crude oil fell $-1.71 or -2.11% at $79.28

- Gold fell $-10.04 or -0.53% at $1891.60. The price is trading at its lowest level since March 15 and as close now below its 200 day moving average for the 2nd day in a row at $1906.26.

- Silver fell -10.5 cents or -0.47% at $22.40

- Bitcoin is trading back below the $29,000 level at $28,925

In the US stock market, major indices fell for the 2nd consecutive day. The NASDAQ index which fell around -1.14% yesterday fell another -1.15% today:

- Dow industrial average fell -180.65 points or -0.52% at 34765.75

- S&P index fell -33.53 points or -0.76% at 4404.32

- NASDAQ index fell -156.43 points or -1.15% at 13474.62

- Russell 2000 was the worst performer with a decline of -24.23 points or -1.28% at 1871.51