- Prior 42.6

- Services PMI 48.4 vs 49.8 expected

- Prior 49.6

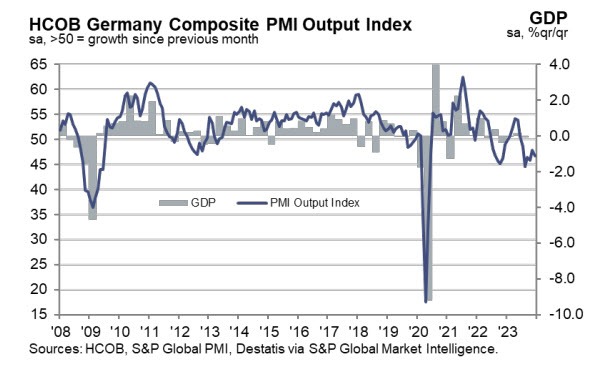

- Composite PMI 46.7 vs 48.2 expected

- Prior 47.8

It's a wake up call for the euro as traders are reminded that the economy is indeed headed for a recession to wrap up the 2023 year. These are some poor figures overall and points to continued struggles in two of Europe's largest economies. Again, it's not a vote of confidence to the ECB and may pressure them into cutting rates sooner than they would like. HCOB notes that:

"If you are on the hunt for gifts right now, you will not strike gold in the latest PMI survey for Germany. What you will find instead is an increasing number of companies reporting a reduction in output in both the service and manufacturing sectors. This confirms our view of a second consecutive quarter of negative growth by the year's close, driven by the manufacturing sector. The less-than-encouraging development could be linked to the constitutional court ruling and the subsequent discord over the 2024 budget. This has injected a significant dose of uncertainty regarding potential new burdens for the economy.

“Despite a recent upturn in the manufacturing stocks of purchases index over the previous two months, December brought a setback. This does not necessarily spell doom for the inventory cycle's potential turnaround next year, but it does hint that the journey to recovery might be bumpier than previously thought.

“In manufacturing, new orders continue to contract rapidly, marking the twenty-first consecutive month of decline. However, the index is on an upward trajectory, fuelled in part by a reduced drag from export orders. Notably, after seven months of pessimism, companies have shifted into optimistic territory regarding future output. This aligns with our perspective that the manufacturing sector is poised for a growth recovery next year.

“In the realm of services, the economic landscape is still dominated by the gloomy hues of stagflation. Output has contracted for the third consecutive month, while input prices are on the rise at a pace mirroring that of November. Interestingly, companies have managed to hike their selling prices even more rapidly than in previous periods. This outcome serves as a stark reminder of the lingering risks to the inflation outlook, despite a substantial overall reduction in official consumer price inflation in recent months."