The Philadelphia Fed nonmanufacturing activity in the region declined in July, as reported by the firms in the Nonmanufacturing Business Outlook Survey. Key indicators such as general activity at the firm level, new orders, and sales/revenues turned negative. The full-time employment index also suggested a decline in employment. Both price indexes showed continued overall price increases, remaining near non-recession averages. Despite the decline, firms still expect growth over the next six months, though these expectations are less widespread.

Below is a summary of the data:

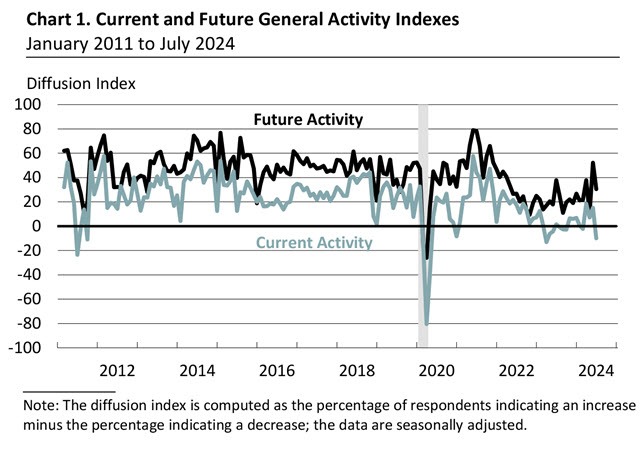

- The diffusion index for current general activity at the firm level turned negative, dropping from 15.1 in June to -10.0, the lowest since April 2023.

- 31% of firms reported decreases, 21% reported increases, and 44% reported no change in activity.

- The new orders index turned negative, falling from 6.7 to -7.1, with 22% of firms reporting decreases and 15% reporting increases.

- The sales/revenues index fell 18 points to -3.5, with 25% of firms reporting decreases and 22% reporting increases.

- The regional activity index dropped 22 points to -19.1, the lowest reading since December 2020.

Employment details:

- Firms reported a decrease in full-time employment, with the full-time employment index falling 20 points to -4.9, its first negative reading since June 2023.

- 19% of firms reported decreases in full-time employment, 14% reported increases, and 66% reported no change.

- The part-time employment index declined from 13.1 to 4.0.

- 63% of firms reported steady part-time employment, 15% reported increases, and 11% reported decreases.

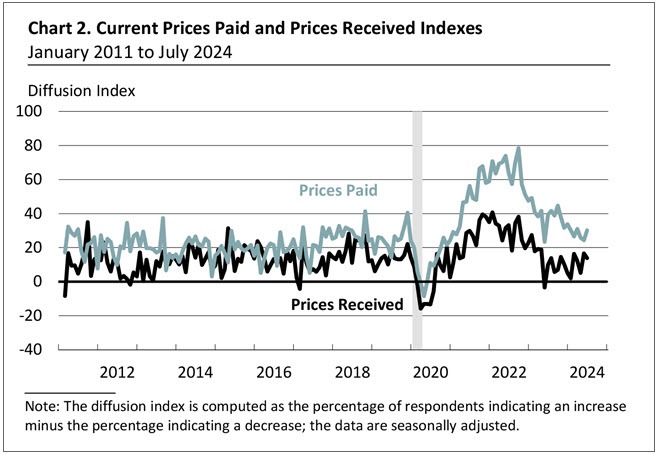

Prices details were mixed with prices paid higher but prices received lower:

- Price indicator readings suggest continued increases in input prices and prices for firms' own goods and services.

- Both price indexes were near their long-run averages.

- The prices paid index rose 6 points to 30.2.

- 32% of respondents reported higher input prices, 2% reported decreases, and 59% reported no change.

- The prices received index declined from 16.6 to 13.9.

- 23% of firms reported increases in their own prices, 9% reported decreases, and 59% reported no change.

In special questions this month, firms were asked about changes in wages and compensation over the past three months, as well as their expected changes to various input and labor costs for 2024.

- Almost 30% of firms reported increased wages and compensation in the past three months, 68% reported no change, and 2% reported decreases.

- 60% of firms reported not adjusting their 2024 budgets for wages and compensation since the start of the year.

- 18% of firms are planning to increase wages and compensation more than originally planned.

- 16% of firms are planning to increase wages and compensation sooner than originally planned.

- Firms expect higher costs across most expense categories in 2024.

- Median expected increases were in line with or slightly lower than expectations when last asked in April.

- Firms expect somewhat lower increases in costs for wages, intermediate goods, and nonhealth benefits compared to April.

- Expectations for increases in total compensation (wages plus benefits) costs remained at a median of 4 to 5%.