- Prior +2.3%

- HICP +1.7% vs +1.9% y/y expected

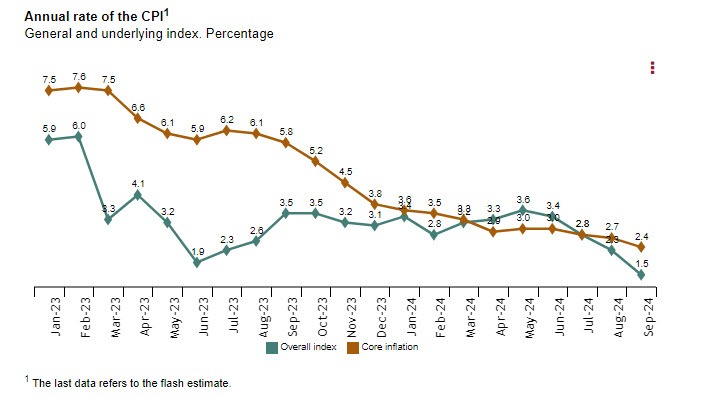

- Prior +2.4%

This adds to the French data from earlier and reaffirms softer price pressures towards the end of Q3. Core inflation is also seen easing further to 2.4%, so that's another positive development. And all of this just rebuffs expectations that the ECB might indeed cut rates by 25 bps next month.